In January, we published our 2021 Economic Outlook. A continued rebound in U.S. and regional economic growth seemed likely then. Market expectations were cautiously optimistic supported by accommodative monetary and fiscal policies. At midyear, the economy is poised to surpass pre-pandemic levels. The stock market has shown amazing resiliency, while fixed income returns remain muted.

What might be next for the economy and markets? This midyear outlook attempts to answer this question by reexamining the economic conditions both nationally and locally and assessing the current market environment.

U.S. Economy

Economic Growth

We identified three economic scenarios in the January Outlook – our base case and an upside and downside forecast. These scenarios were informed by four key variables:

- The extent of the virus' resurgence this past winter

- The status of the job market and consumer spending

- The efficacy, adoption, distribution, and safety of COVID-19 vaccines

- How the political transition affects business and consumer confidence

Our base case proved too conservative. The upside scenario unfolded in the first half of 2021, as the pace of the economy was stronger than anticipated. In the U.S., economic strength was fueled by the following drivers:

- The spread of the virus slowed in the first quarter and lockdowns were avoided

- The job market and consumer spending bounced back quickly

- Vaccines became widely available early in the year

- Additional stimulus (and the prospect of more) elevated consumer and business confidence

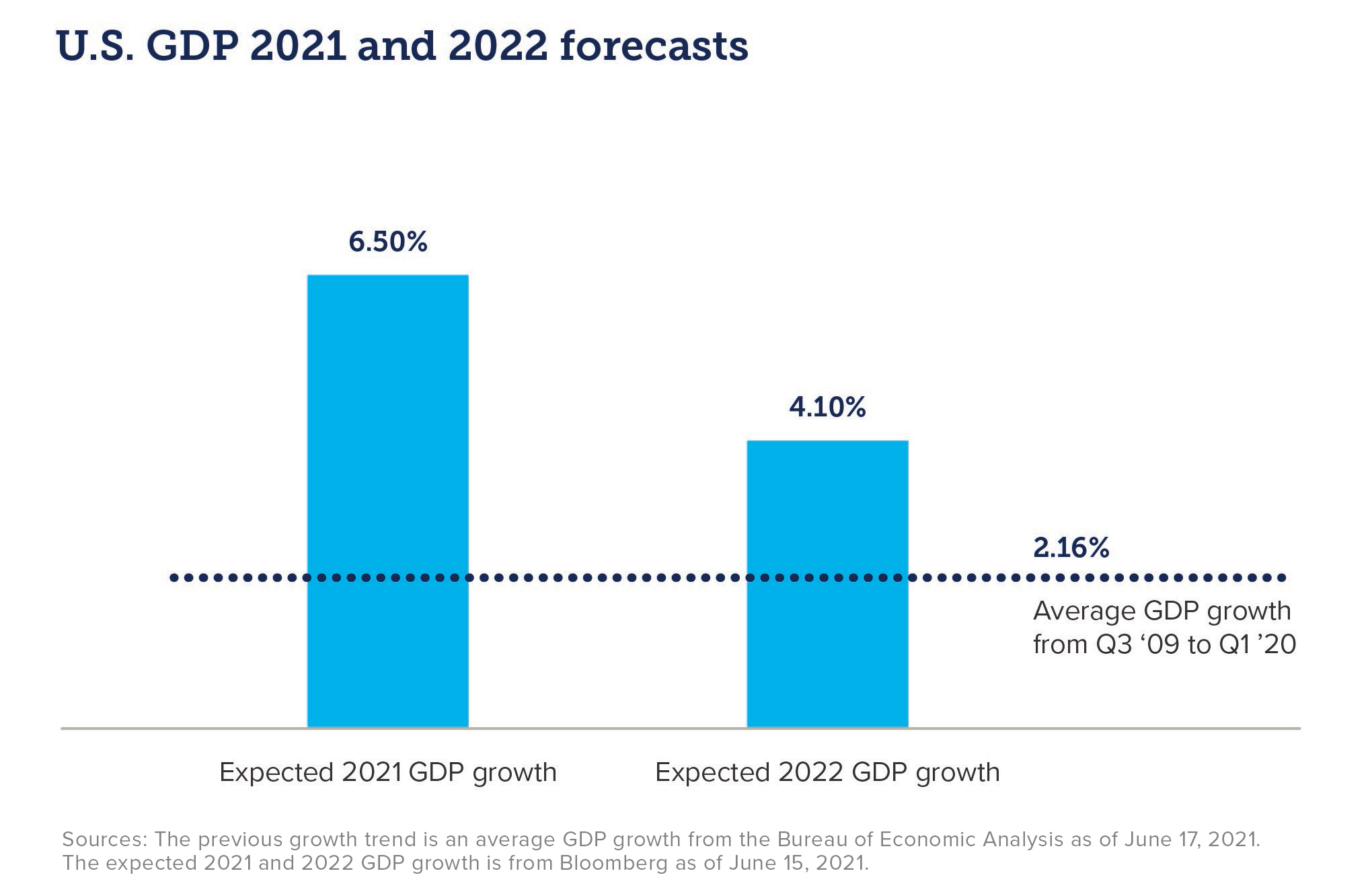

As we look to the second half of the year, economic prospects remain bright. Consensus estimates for U.S. GDP growth are 6.5% and 4.1% for 2021 and 2022, respectively. These estimates place the U.S. economy surpassing its pre-COVID growth trend midway this year, and much quicker than previous recoveries as illustrated below.

Inflation

Earlier this year, we noted that if our most optimistic scenario unfolded, unanticipated increases in inflation could emerge. Such has been the case, as the Consumer Price Index (CPI) in April jumped 4.2% year over year, followed by a 6.2% increase in May. Disruption in global supply chains have led to shortages in lumber, home inventories, used cars, and many other goods and services. Constrained supply met with strong demand have produced higher levels of inflation than expected.

Will these elevated price increases continue or subside? The Fed believes these inflation spikes will be transitory. We tend to agree with this view. The secular forces that have kept inflation low for years, including globalization and rapid technological change, remain in place for the foreseeable future. Also, slack in the labor market historically has helped contain inflation. However, given structural shifts, policy changes, and attitudinal differences in the labor market following the pandemic, we are cautious to draw too strong of inferences from historical patterns. Nevertheless, the overarching secular forces, combined with the Fed’s mandate to have price stabilization, make an inflationary spiral unlikely.

Regional Economies

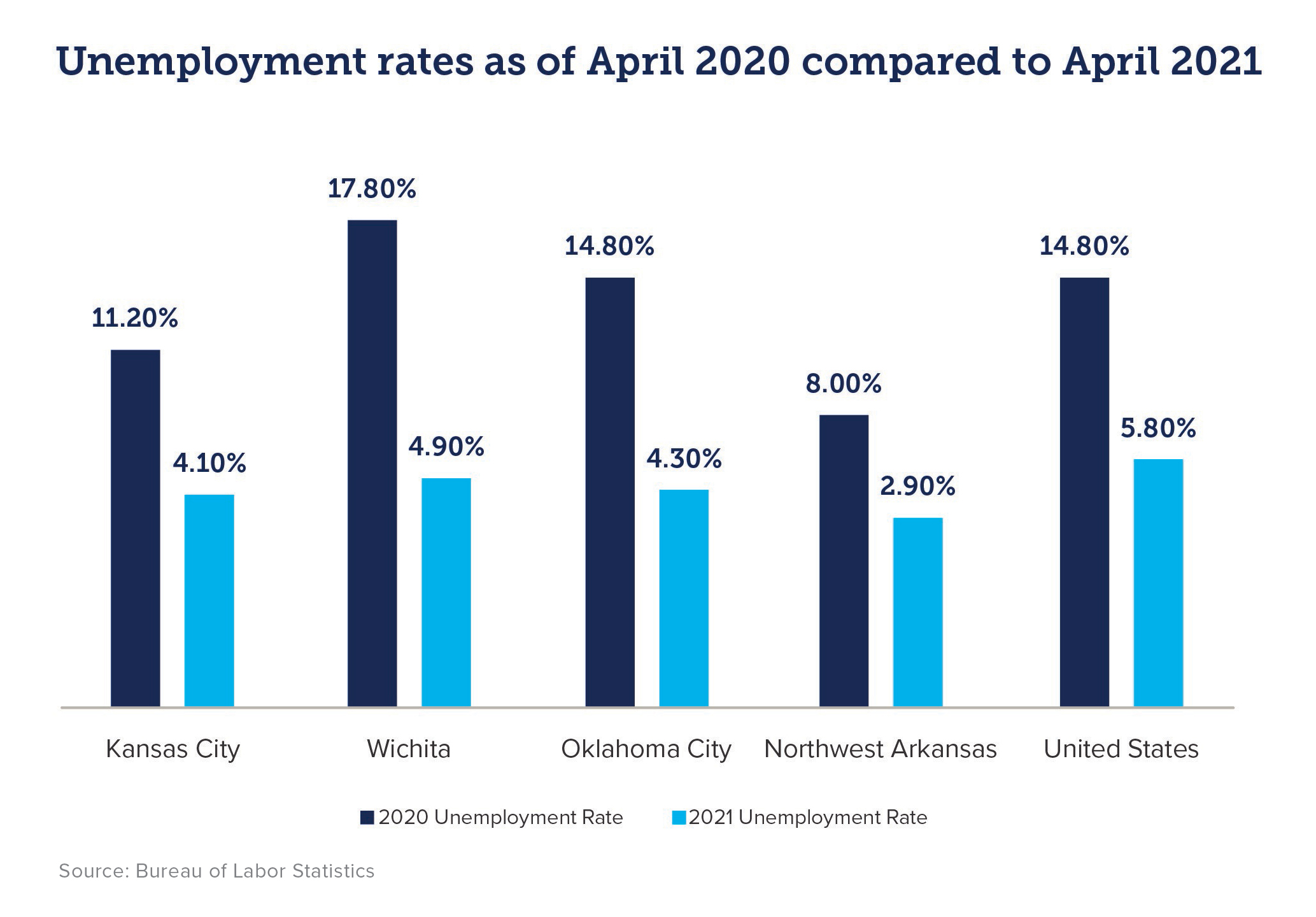

Kansas, Oklahoma, and Arkansas also experienced strong recoveries. Labor markets in these local regions continued to make gains during the first half of 2021 as illustrated by the chart below. In fact, there are more job openings than eligible candidates in many industries across our region, making it hard for employers to fill job postings. Northwest Arkansas’ unemployment rate as of April 2021 was below 3%, and KC’s and OKC‘s hovered around 4%. Wichita’s unemployment rate as of April 2021 came in at 4.9%, not quite as strong of reading as the other regional markets but better than the U.S. unemployment rate.

Across each of our regional markets, housing remains very hot, with supply and demand factors indicating that this trend is not going to change any time soon. Similarly, construction is expected to remain strong in our regional markets through the end of the year. In Wichita, commercial aerospace demand is increasing faster than initially expected, which is good news for local aircraft manufacturers and their suppliers. The rise in energy prices bodes well for the OKC market, helping to drive this region’s economy forward during the second half of this year. Furthermore, both NWA and KC economies should benefit from strong consumer demand and serving as regional transportation hubs as economic activity continues to expand.

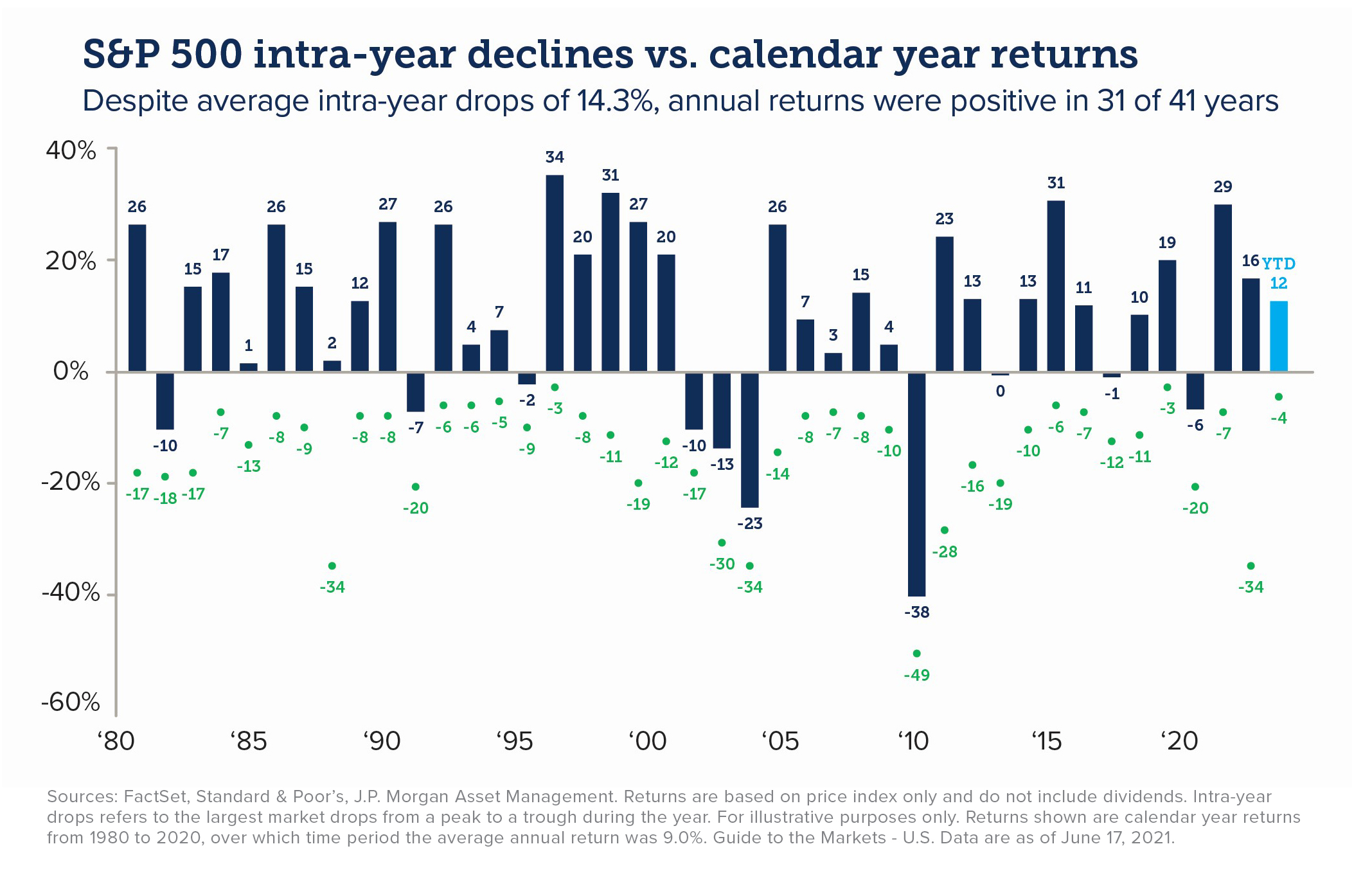

The S&P 500 Index hit all-time highs in the second quarter, while fixed income faced headwinds from higher rates and inflation concerns. As we enter the second half of the year, our outlook for investment returns in 2021 and beyond remains cautiously optimistic.

Equities

U.S. equities posted double-digit gains this year and nearly triple-digit gains from March 2020 lows. Despite this exceptional, near-term performance in the stock market, we believe equities may be poised for further advancement in 2021. The lingering impact of unprecedented levels of fiscal stimulus, central banks’ accommodative monetary stances across the globe, and the prospects of strong corporate earnings for the remainder of this year and next year could further buoy equity markets – both domestically and internationally. However, markets may experience heightened volatility if the Fed signals its intent to raise rates sooner than anticipated given the strength of the economy. During the first half of 2021, we saw a rotation from growth-oriented stocks to more value-oriented securities and from large-cap companies to small-to-mid-sized stocks. These trends may continue.

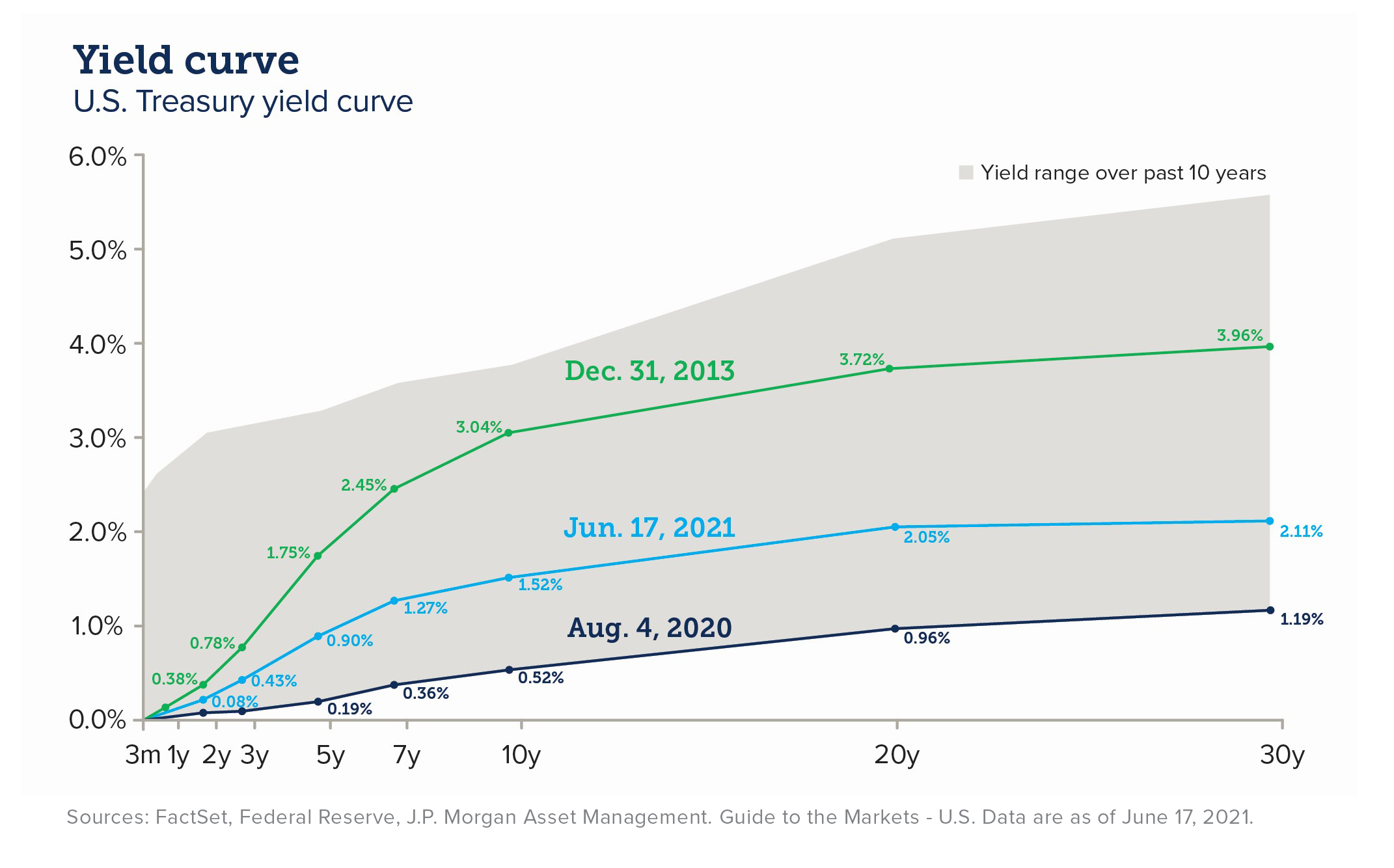

Fixed income

Bond returns were flat to slightly negative during the first half of 2021. Intermediate and long-term Treasury yields rose during the year as the economy gained steam and higher inflation expectations emerged. This rising rate environment depressed fixed income returns. Moreover, as investors continued their search for yield, riskier fixed income assets such as high yield became more expensively priced compared to their historical norms. Similarly, prospects of higher taxes led to money pouring into municipal bonds, keeping yields low and valuations elevated. Such an environment leaves little room for near-term upside for many of the fixed income sectors. Accordingly, we believe fixed income investors should generally hold shorter duration bonds and utilize actively managed fixed income strategies. Despite our outlook for low fixed income returns in the near term, bonds continue to play an important role in investor portfolios, providing diversification benefits and downside protection if higher volatility reemerges in the equity markets.

With equity markets hitting all-time highs, fixed income sectors appearing expensive, and inflation concerns surfacing, what actions should investors take now? Fortunately, the key to successful investing is not predicting the future. Nor is it reacting to the ever-changing headlines. We believe adhering to time-tested strategies – informed from past experiences and designed to reach tomorrow’s goals – is a wise approach. Below are four of these proven strategies for investors to consider as we enter the second half of 2021.

1. Don’t confuse speculation with investing

2021 has brought stories of meme stocks soaring to crazy heights and cryptocurrencies as the latest rage. A few speculators have and will make money from these high-flying stocks and digital currencies. But many people will find themselves on the wrong side of these trades. Don’t fall for the temptation to get rich quick. Patience and discipline are virtues practiced by successful investors.

2. Minimize the impact of taxes on portfolio returns

Both corporate and personal taxes will likely increase. Included among the proposed tax changes is an increase in capital gains rates for certain taxpayers. Applying tax-smart strategies, such as proactively harvesting losses to offset gains and optimizing the location of assets among taxable, tax-deferred, and tax-free accounts, will help taxable investors keep more of what they earn. Active tax management will become an increasingly important component of maximizing investor returns amid the backdrop of higher taxes.

3. Maintain cash for liquidity, but not for market timing

The adage “Cash is King” may not be the most prudent strategy in a low-rate environment and the prospects of rising inflation. Certainly, investors with near-term spending requirements should maintain sufficient cash savings to cover these expenses. However, keeping cash on the sidelines to wait for an opportune time to invest may be a costly approach. Our experience suggests that clients who maintain a disciplined, long-term approach to investing often are better positioned to achieve their financial goals than those who try and time the market’s peaks and troughs.

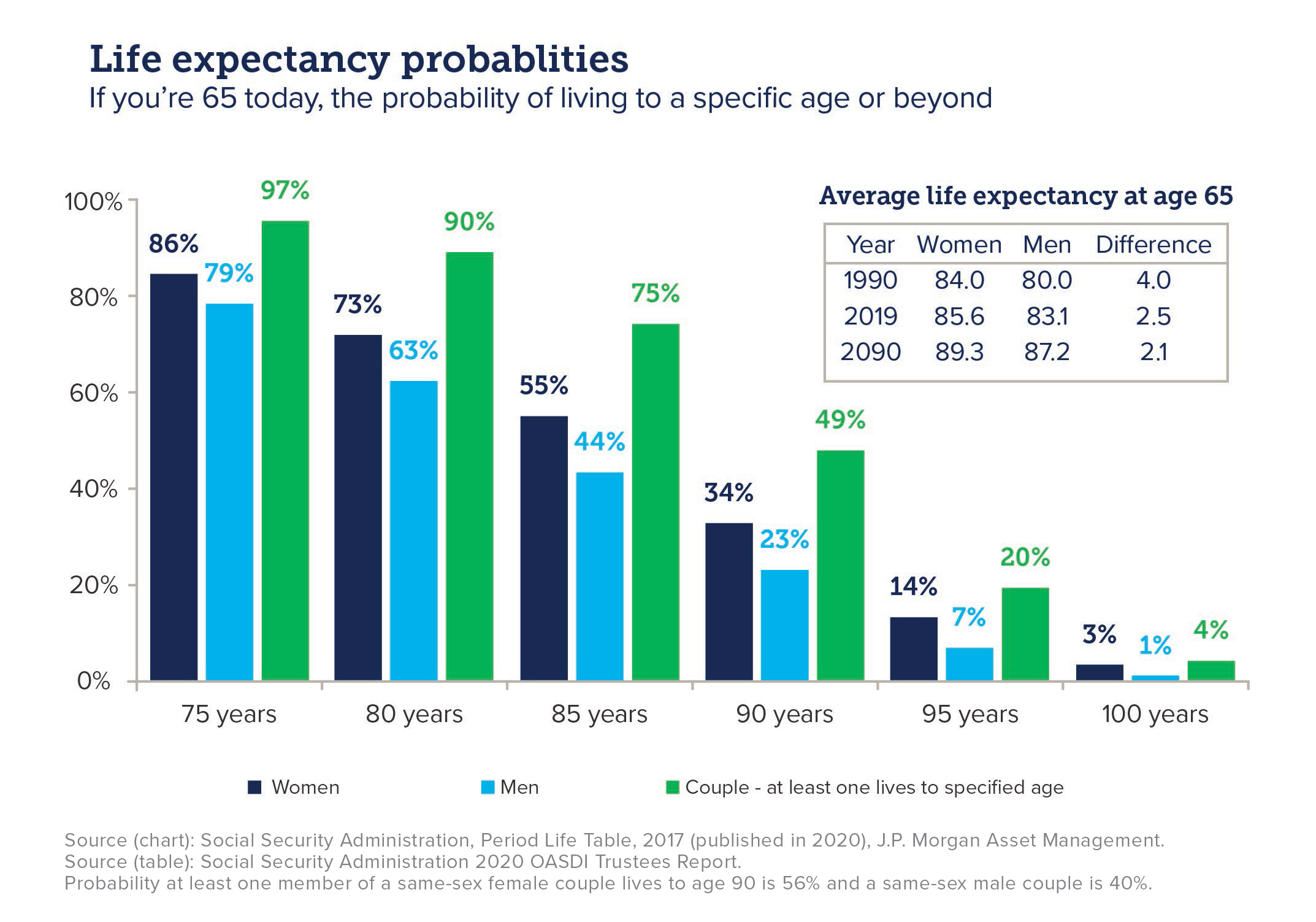

4. Plan on living a long time

The probability of one member of a 65-year-old couple living at least another 25 years is nearly 50%. Accordingly, investors should make sure they have sufficient savings for a long life and design portfolios with longevity in mind. We have data-driven tools to help investors plan appropriately for a long lifespan and end-of-life healthcare costs. Visit with your advisory team to learn more about our personalized longevity assessment and how it relates to your financial plan.

The INTRUST 2021 Midyear Outlook is the consensus of the INTRUST Investment Strategy team and are based on third-party sources believed to be reliable. INTRUST has relied upon and assumed, without independent verification, the accuracy and completeness of this third-party information.

INTRUST makes no warranties with regard to the information or results obtained by its use and disclaims any and all liability arising out of the use of, or reliance on, the information.

The information presented has been prepared for informational purposes only. It should not be relied upon as a recommendation to buy or sell securities or to participate in any investment strategy. The Midyear Outlook is not intended to, and should not, form a primary basis for any investment decisions. This information should not be construed as investment, legal, tax or accounting advice. Past performance is no guarantee of future results.

| Not FDIC Insured | No Bank Guarantee | May Lose Value |

Posted:

07/12/2021

Category:

Recommended Articles