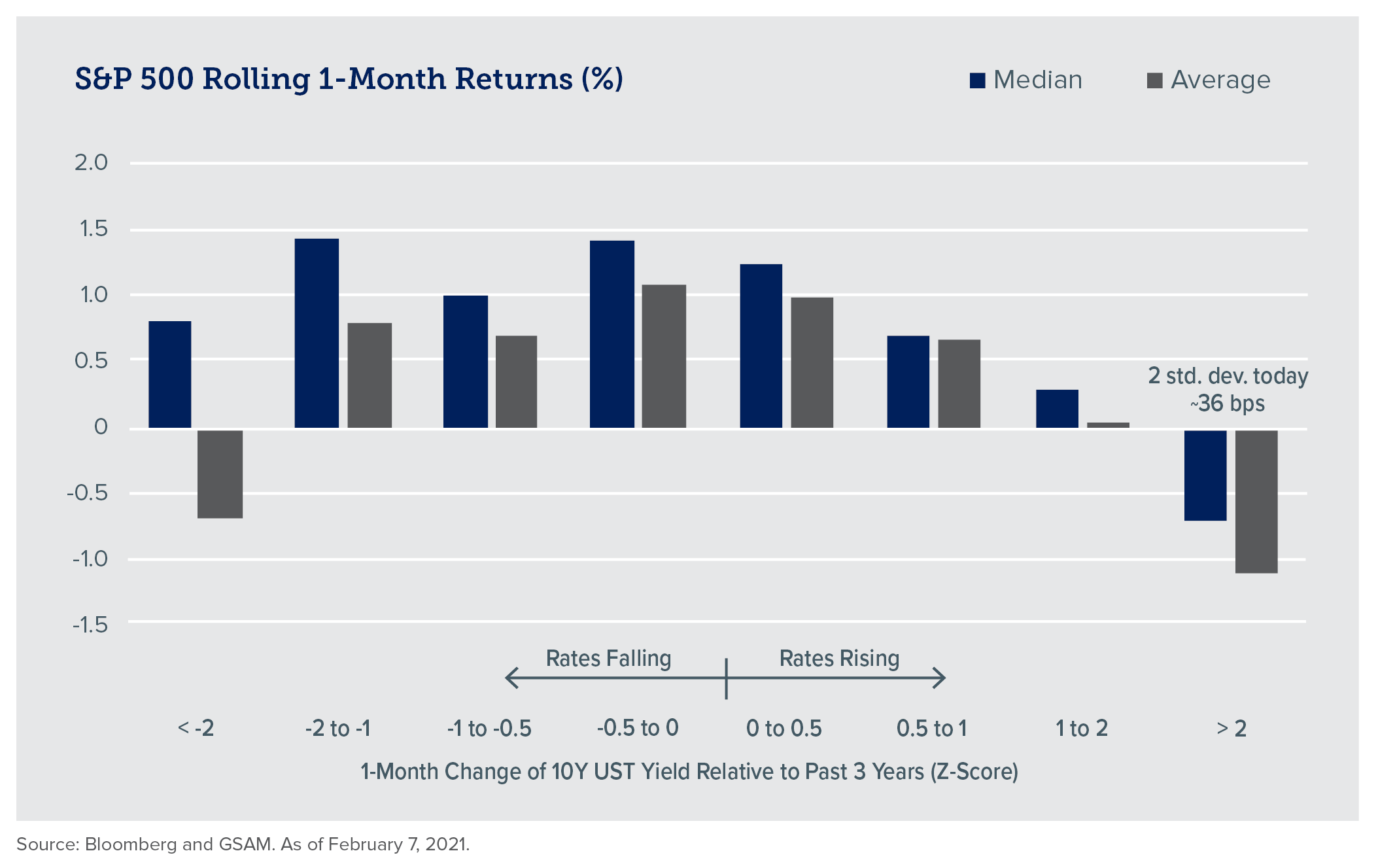

Interest Rates and Inflation

In the INTRUST 2021 Economic Outlook, our view of the economic recovery occurring throughout 2021 is based on several factors, not the least of which is the mitigation of the negative impacts of COVID-19. As the economy improves, the likelihood of inflation and rising interest rates will play an important role in market performance.

The Fed’s very accommodative policies pushed Treasury yields to historically low levels and indirectly boosted equity valuations. Further, multiple stimulus packages from Congress have sharply increased the supply of money, which can lead to an inflationary environment. If long term average inflation rises above the Fed’s target rate, they will likely relax some of their accommodative policies, allowing yields to continue to increase. The speed at which yields increase has shown to influence the performance of equities.

Moderate rate changes tend to have little effect on equity performance. However, rapid increases (>2 std dev in a 1-month period) have shown to be a detractor to equities.

U.S. Economy Opening in Waves - Update

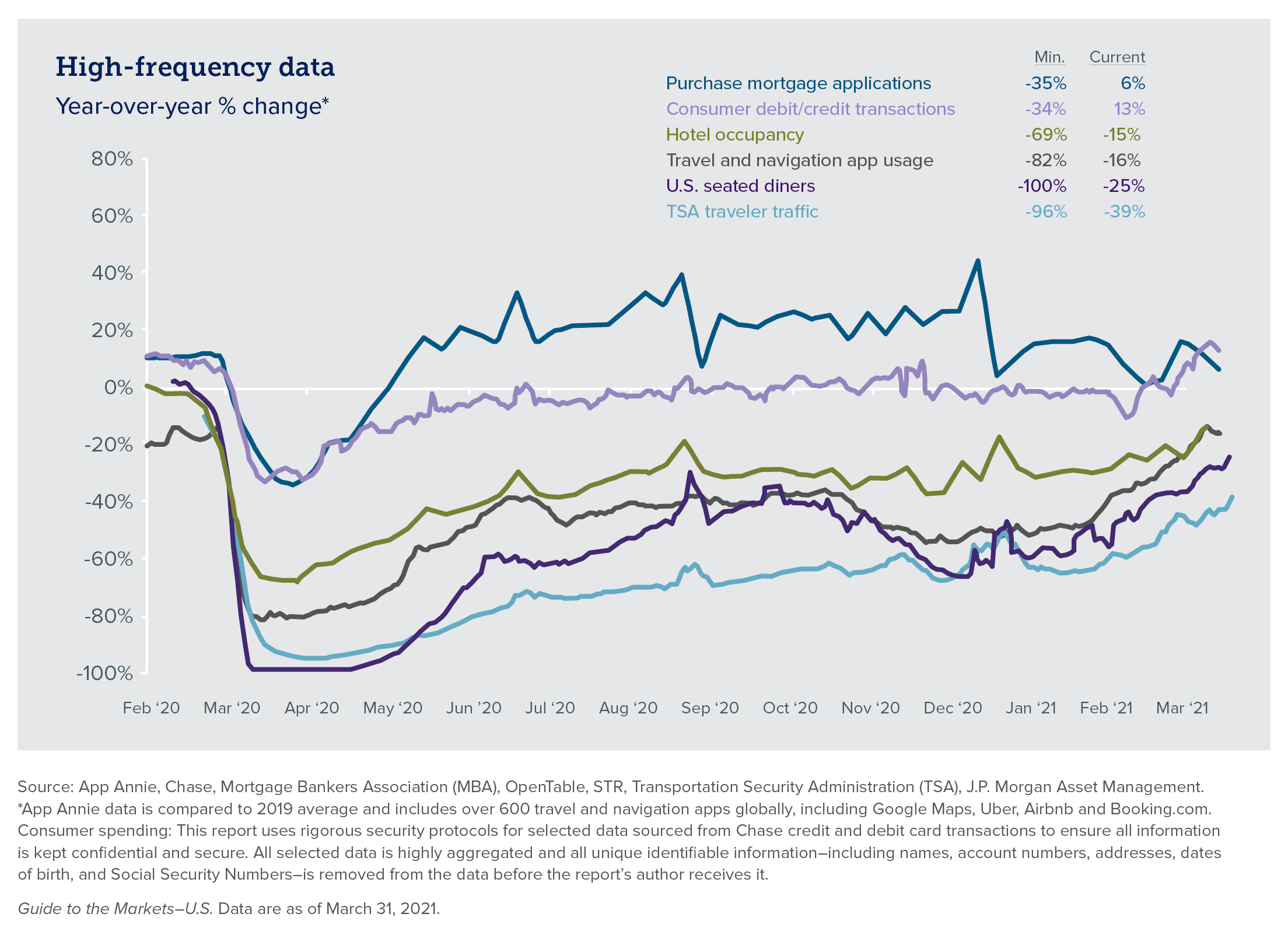

In our 3rd Quarter 2020 Quarterly Perspectives, we provided data showing that not all sectors of the US economy were recovering at the same rate. That data has been updated below and continues to show diversity in sector recovery. Many of the under-performing sectors rely on in-person contact and further improvement in these areas will hinge primarily on widespread acceptance of the COVID-19 vaccines and attainment of herd immunity to the virus.

The recently passed $1.9T stimulus package as well as the additional round of Paycheck Protection Program (PPP) loans should further boost the pace of economic recovery.

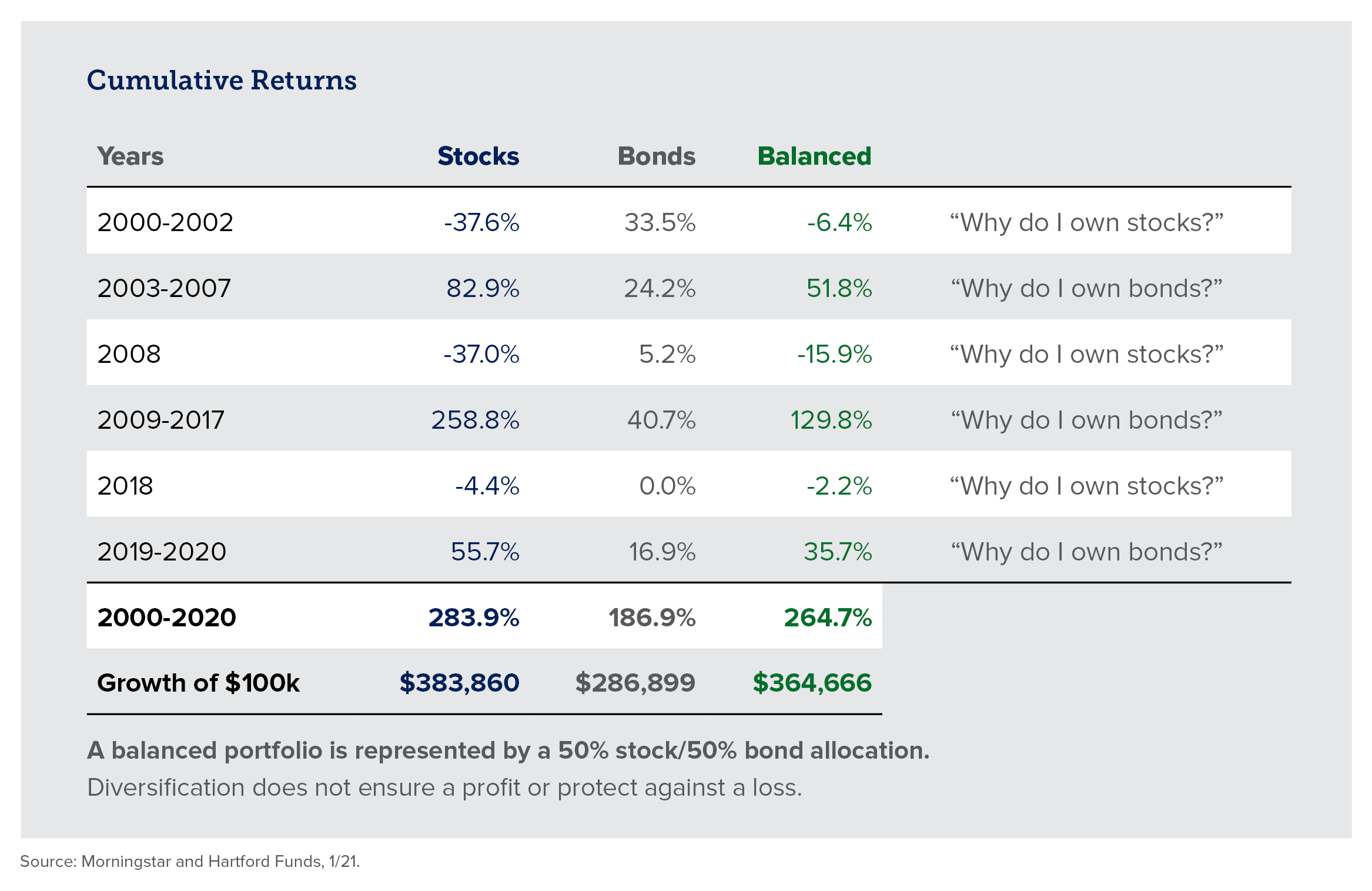

A Balanced Approach Matters

Periods of high market volatility often cause investors to get nervous and seek perceived advantage by making significant allocation changes in their portfolios. However, overreacting to short term volatility often hurts investors in the long term. We believe a diversified portfolio based on long term goals, coupled with active tax management, will reward the disciplined investor.

Economy/Financial Markets

- Distribution of Covid-19 vaccines and attainment of herd immunity will continue to support consumer confidence.

- Fed committed to maintain accommodative policy to support the economy until data (particularly inflation and unemployment rate) support a change.

- The Fed Funds Futures market is forecasting low likelihood of any further rate changes throughout 2021.

- The recently approved $1.9T stimulus package and any future government stimulus will continue to play an important role in the recovery.

- The strength of the economic rebound will largely depend on an improvement in business confidence and/or consumer confidence levels.

- Continuation of the Paycheck Protection Program (PPP) loans will provide needed support to businesses struggling to maintain current staffing levels.

- Inflation expectations remain at or below the Fed’s target level of 2% but could move higher quickly as the economy heats up.

Growth Assets

- Equity market performance in 2020 was heavily influenced by a handful of large growth stocks but recent performance data reflects a rotation to value.

- Attractive valuations exist in parts of the markets, particularly in US Large Cap Value, US Mid- and Small-Cap, and Emerging Markets.

- Volatility levels have tempered from historic highs in 2020 and are approaching average levels.

- Corporate earnings, which came under pressure from the business disruption caused by coronavirus concerns, are showing signs of rebound.

- Emerging Markets performance is heavily influenced by the strength of the US Dollar. Risks associated with trade and the spread of the coronavirus have hampered EM near-term prospects. Longer-term Emerging Markets continue to look attractive from a risk/return standpoint.

- Historically, markets have performed well coming out of a recession.

Defensive Assets

- A potential rising-rate environment will be a key driver of fixed income performance.

- Treasury rates have risen in the upper end of the curve, providing opportunities for actively managed bond portfolios.

- Corporate and high-yield bonds have seen spreads widen relative to Treasury yields, but have provided better downside protection than equities during market corrections.

- An environment of higher levels of interest rate volatility is likely to continue.

The INTRUST Quarterly Perspectives are the consensus of the INTRUST Investment Strategy team and are based on third party sources believed to be reliable. INTRUST has relied upon and assumed, without independent verification, the accuracy and completeness of this third party information.

INTRUST makes no warranties with regard to the information or results obtained by its use and disclaims any and all liability arising out of the use of, or reliance on, the information.

The information presented has been prepared for informational purposes only. It should not be relied upon as a recommendation to buy or sell securities or to participate in any investment strategy. The Forward–Looking Perspectives are not intended to, and should not, form a primary basis for any investment decisions. This information should not be construed as investment, legal, tax or accounting advice. Past performance is no guarantee of future results.

| Not FDIC Insured | No Bank Guarantee | May Lose Value |

Posted:

04/13/2021

Category:

Recommended Articles