Personal Banking

Personal Banking

2020 Economic Outlook

The U.S. economy will likely enter its 12th year of economic expansion in 2020, continuing the longest growth period in history. While we anticipate GDP and regional economies to slow, consumer strength remains solid, but not without critical factors that may influence economic and market outcomes in 2020. As a practice to continually provide relevant and insightful information, our team of commercial banking and wealth management professionals analyzed the economic conditions that businesses and investors face moving into 2020 in our annual Economic Outlook.

2020 Economic and Market Summary

U.S. Economy

- Given the current strength of the U.S. consumer sector, we anticipate the lengthy U.S. economic expansion to continue near a 2% GDP growth rate this year, with a low chance of recession in 2020.

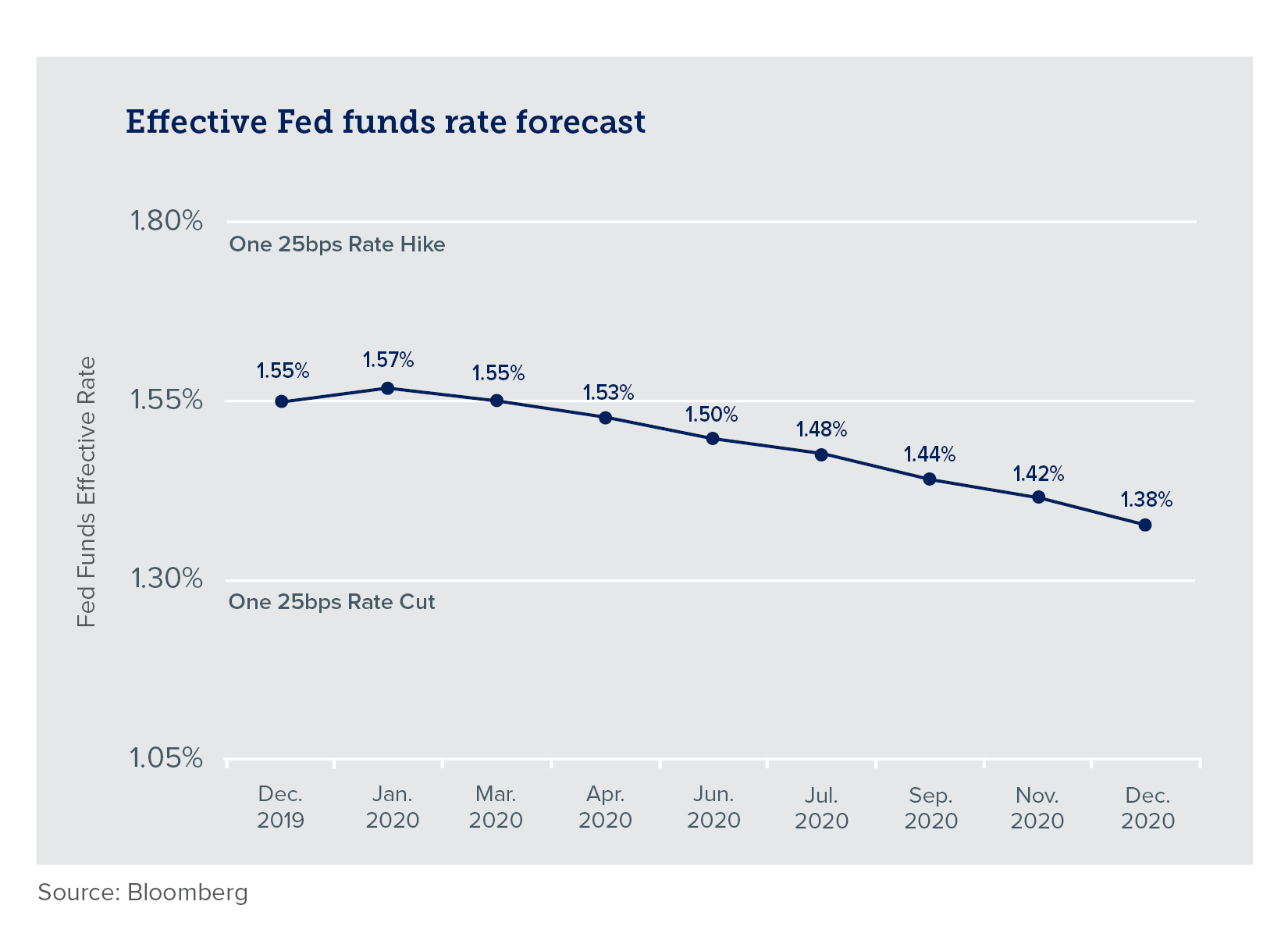

- After lowering rates three times in 2019, the Fed is signaling a halt in cuts this year. We are forecasting rates to remain unchanged in 2020, but the Fed Funds Futures Market suggests one rate cut may occur late this year.

Regional Economies

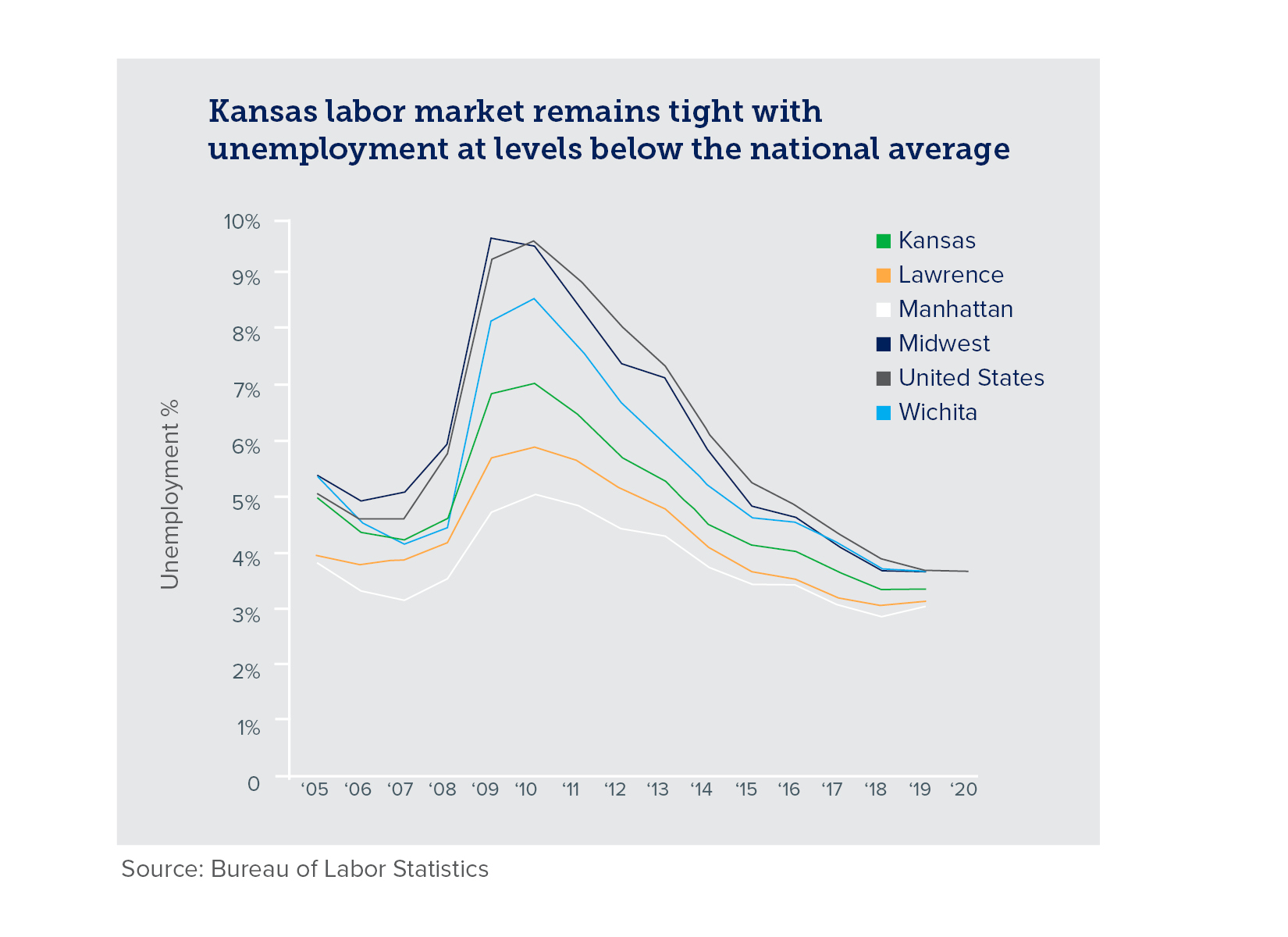

- We expect economic and job growth in Kansas and Oklahoma will slow in 2020, but these regions likely will avoid recession this year.

- Unemployment rates below the national average and low population growth are reasons that economic expansion in Kansas and Oklahoma may be constrained.

Factors to Watch

- Changes in business investment, consumer strength and the global economy are key factors to watch in early 2020.

- Other factors that may influence our national and regional economies include trade policies and the upcoming U.S. elections.

Markets

- Equity and fixed income markets soared higher in 2019, closing out a decade of exceptional market returns.

- Investors should reset return expectations for the next decade, anticipate more volatility leading up to November's elections and commit to a disciplined investment strategy for reaching their long-term goals.

U.S. Economy

In June 2020, the U.S. economy should enter its 12th consecutive year of positive GDP growth — the longest expansion in U.S. history — but is the end in sight? While rhetoric suggests an impending recession lies in 2020, we believe the probability of a recession remains low, given the current strength of the U.S. consumer sector. Nonetheless, risks are increasing as the economy will likely decelerate from 3% growth to 2% growth or less this year.

Consumer Strength

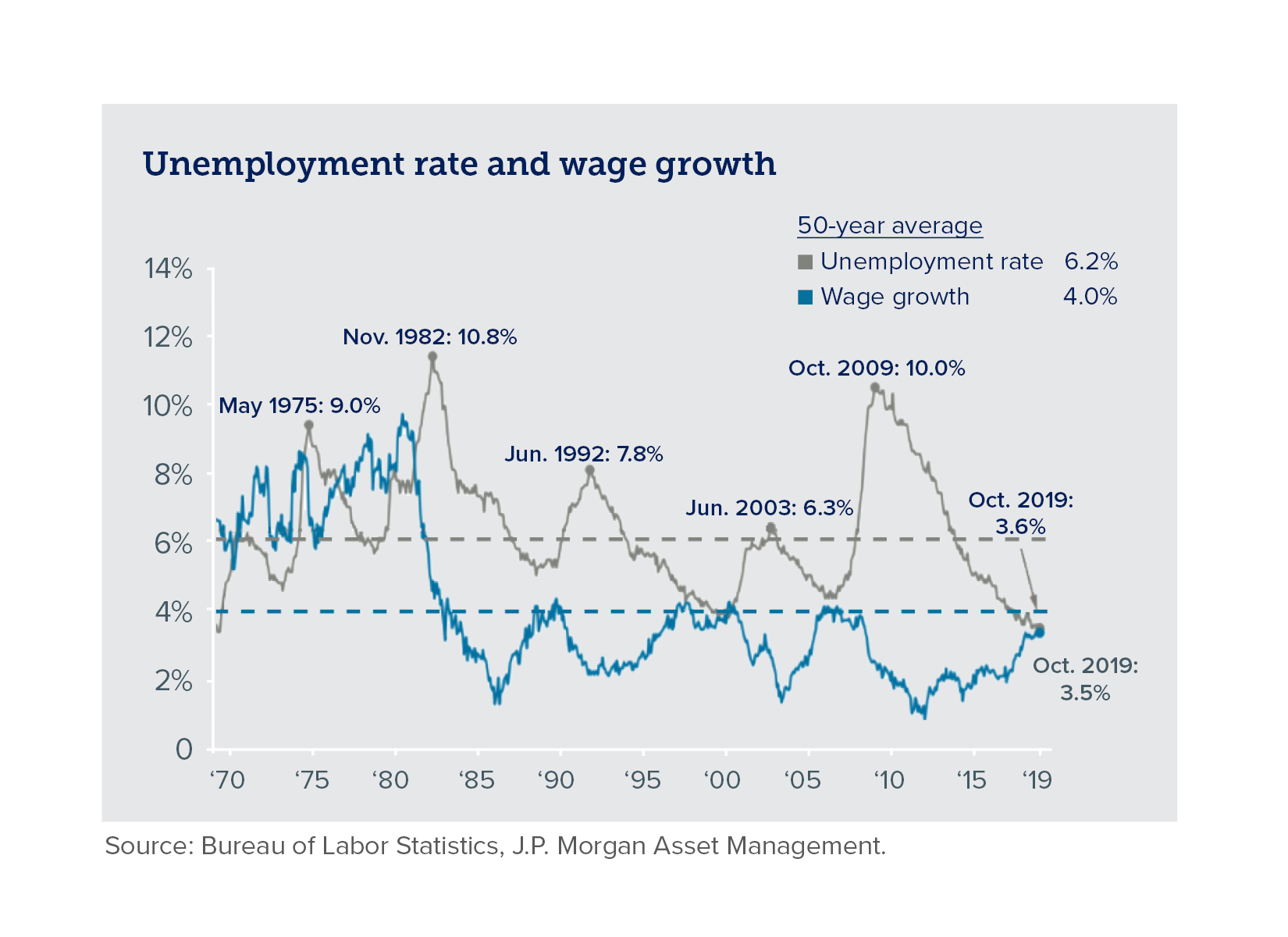

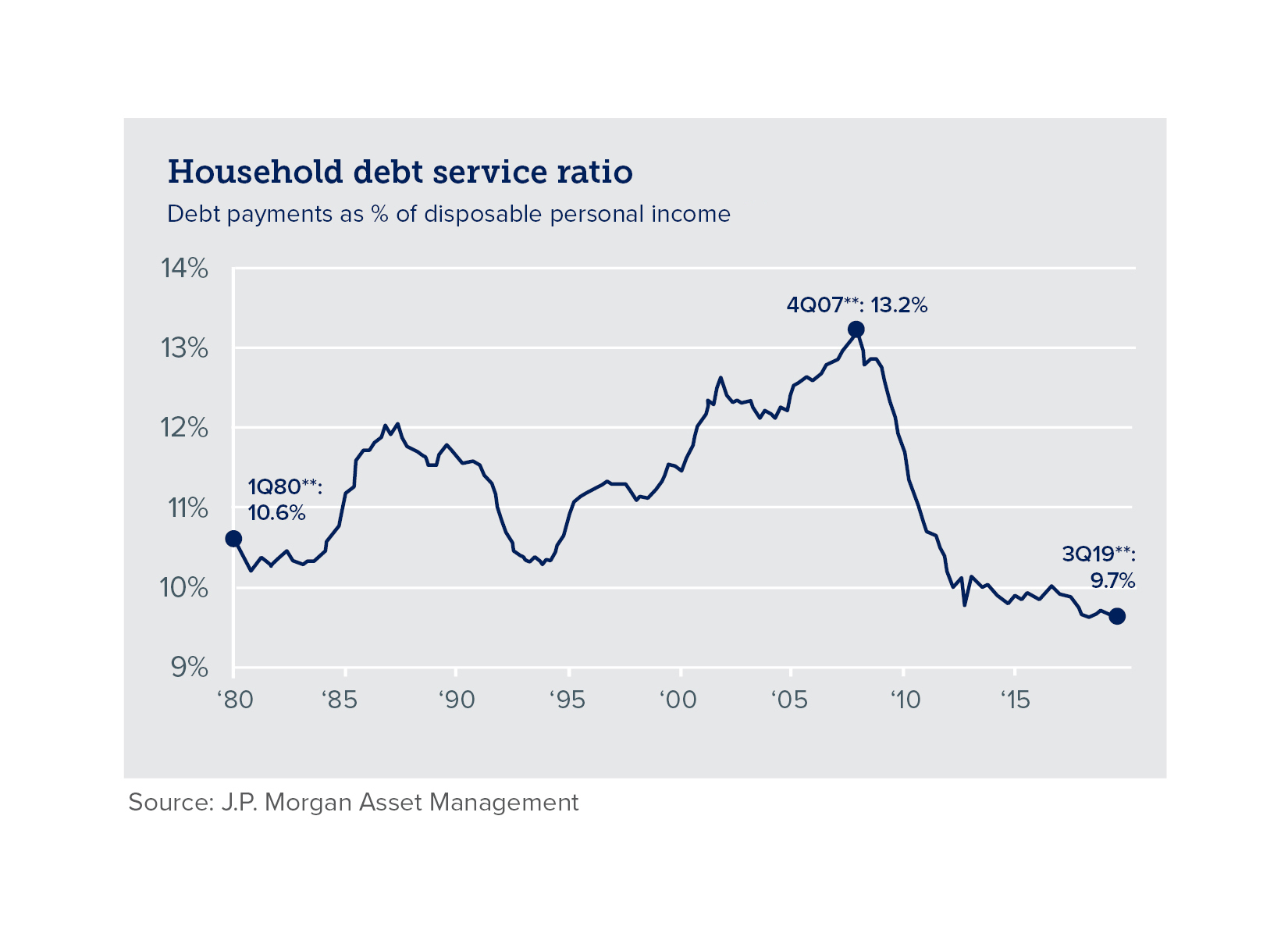

Consumption indicators remain of paramount importance to U.S. economic growth, given that consumers drive more than two-thirds of our economy. To that end, we anticipate the consumer sector to remain on solid footing in 2020. Household spending should be supported by continued low unemployment and wages growing faster than core inflation. Also, household debt service ratios should continue hovering around 40 year lows, while savings rates remain high.

Business Investment

Notwithstanding our expectations of continued consumer strength, downside risks appear to be increasing — namely driven by an anticipated slowdown in business investment. Major capital expenditures will likely remain sluggish as businesses confront the uncertainty of the upcoming U.S. elections and lackluster global growth. Furthermore, it is getting harder for businesses to make money, especially in a service-based economy like the U.S., where a large portion of expenses come from people costs. As economic growth slows, wages rise and productivity gains stall, corporate profit margins will come under mounting pressure. Additionally, small businesses — the heart and soul of the American economy — may be the hardest hit with these challenges.

Fed Policy

July 2019 was a historic month for monetary policy as the Fed reduced the Federal Funds Target Rate by 25 basis points. This move was the first sign of easing since 2008! The Fed further reduced rates in September and October, for a total adjustment of 75 basis points in 2019. While the Fed is currently on pause for further rate cuts, it has not ruled out the possibility for more cuts in 2020. We are forecasting rates to remain unchanged in 2020, but the Fed Funds Futures Market suggests one rate cut may occur late this year.

Regional Economies

Kansas

We anticipate economic growth in Kansas to slow, with job gains likely to fall below 1% in 2020. The state’s unemployment rate should remain below the national average. Moreover, Kansas' population and labor force are growing slowly. The scarcity of workers will constrain economic expansion in the state.

Rural areas are still reeling from agricultural price declines and the retaliatory Chinese tariffs. However, China recently committed to buy a record amount of U.S. agricultural products in 2020 in phase one of the trade deal. This agreement should provide welcome relief to Kansas farmers, who, despite the market facilitation program set up by President Trump to compensate for losses, have been hurt by the Chinese tariffs.

The Wichita metro economy is closely tied to the ebbs and flows of the aerospace industry. In late 2019, two significant aerospace announcements were made that will likely impact the Wichita economy. Foremost, Boeing announced it is temporarily suspending production of the 737 MAX jetliner in 2020. As this action plays out, ripples will be felt throughout the local aerospace supply chain. To soften the effects of the suspension, the state of Kansas is offering support to workers through a shared-work program if there are any reductions in work schedules. One of Wichita’s largest aerospace employers, Textron Aviation, added 1,000 workers both in 2018 and 2019 but announced layoffs at the end of 2019. A bright spot for Wichita is its downtown development. These efforts should continue to gain momentum in 2020, as the city anticipates the opening of its new Triple-A ballpark.

In the Kansas City metro area, businesses are finding it increasingly difficult to hire and keep good people. Even though several colleges and universities are in the area, graduates are taking jobs in faster-growing markets. This export of talent and

the tight labor market will limit Kansas City’s growth potential in 2020. To manage this challenge, companies are looking to foster attractive corporate cultures and enhance employee engagement efforts. Also, some businesses are finding success

in hiring boomerang workers — those who leave the market after college but are willing to return to the Midwest after starting families. Opportunities in the animal health corridor from Manhattan, KS, to Columbia, MO, appear positioned to gain

momentum in 2020 and beyond. One example is Scollar, a smart pet collar company, that recently relocated to Kansas City from California. Kansas City is also a hub for transportation. This sector softened in 2019 but may improve

this year, given the progress being made on trade policy. Construction is another industry that we believe will remain strong in 2020, as well as related fields such as architecture and engineering.

Oklahoma

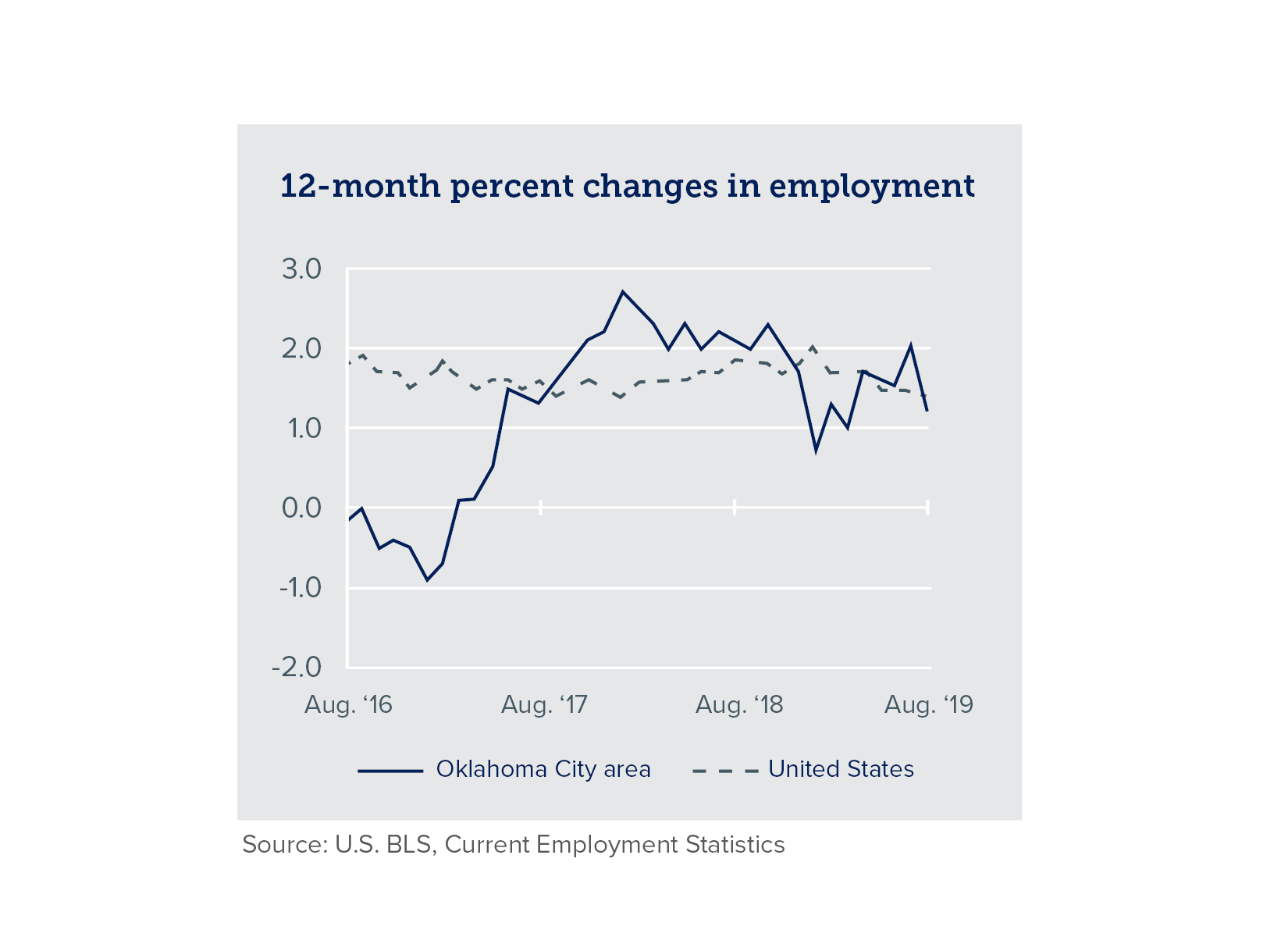

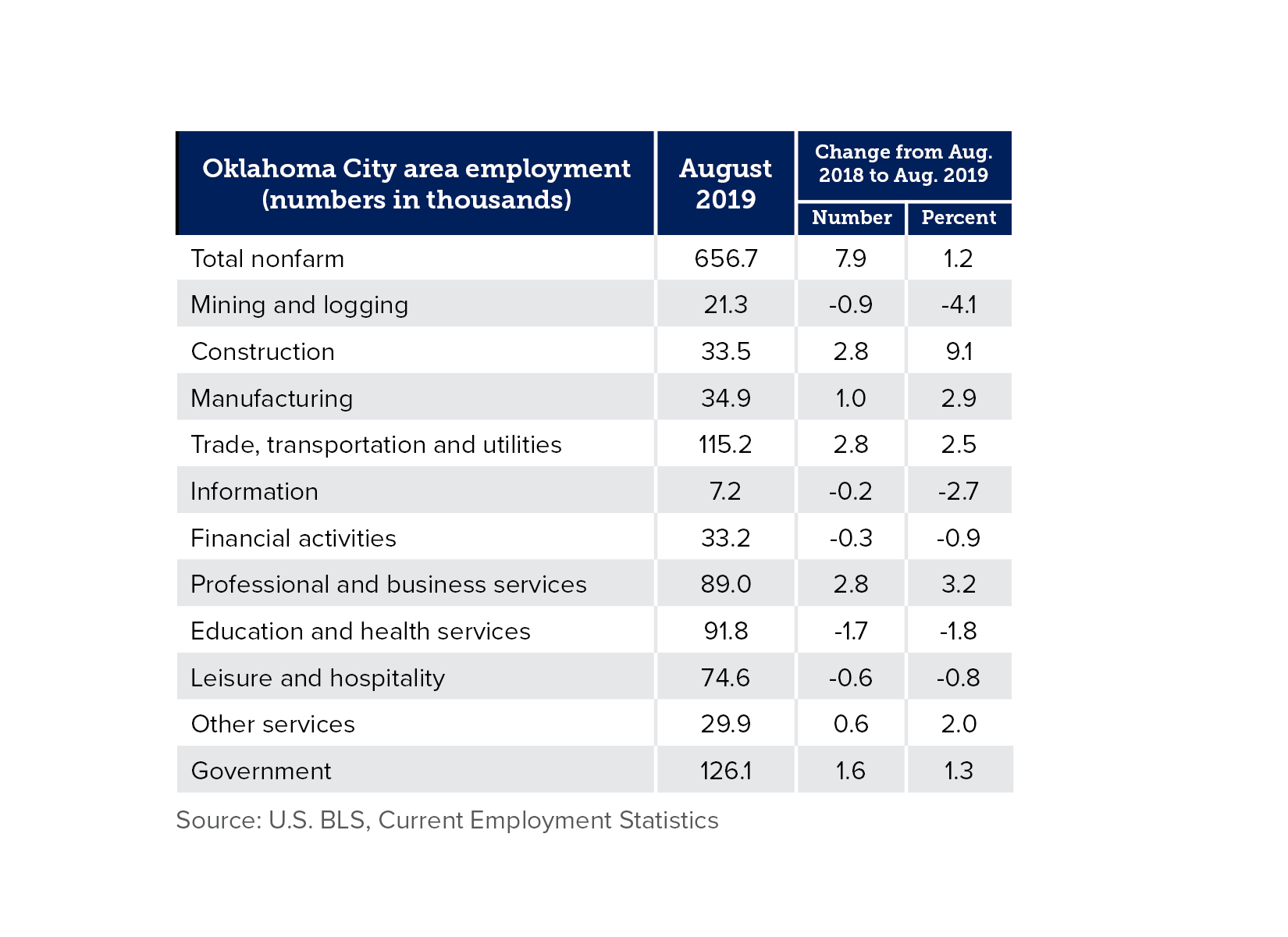

We expect economic growth in Oklahoma to downshift in 2020, with job gains likely to fall below 0.5% this year. Similar to Kansas, Oklahoma’s unemployment rate should remain below the national average. The state’s economy is closely tied to the energy sector and related industries. Low prices of natural gas and mediocre oil prices will likely continue hampering economic growth in Oklahoma. The state's largest employers are located in Oklahoma City, including Chesapeake Energy and Continental Resources. Concerns over Chesapeake’s potential bankruptcy have eased. Still, the company’s growth prospects will be limited as it continues to focus on reducing its rig count and paying off its debt in 2020.

Although the energy sector will continue to significantly impact Oklahoma, the state’s economy is showing promising signs of diversifying its economic base. The aerospace industry is emerging as a leading growth sector for Oklahoma, especially in the Maintenance, Repair and Overhaul (MRO) segment. Oklahoma has the largest government MRO operations at Tinker Air Force Base, along with the nation’s biggest commercial and independent MROs based in Tulsa and Oklahoma City. Moreover, the Federal Aviation Administration’s facilities in Oklahoma City employ more than 6,000 workers, and a new 100,000 square foot unmanned aircraft production facility opened with further production coming online in 2020.

Oklahoma is also attracting more distribution and technology companies. Amazon is hiring about 1,700 people for its warehouse in Oklahoma City. The company intends to add a second distribution center in Tulsa, reflecting Oklahoma’s ideal centralized location as a transportation hub. In 2019, Google announced plans to expand its data center in Oklahoma. Google’s investment in the regional data center totals more than $3 billion, increasing local employment by more than 500 people. These expansion projects, along with others, will keep job momentum going strong in Oklahoma’s construction sector in 2020.

National and Regional Economic Influencers

Although we are forecasting the U.S. and regional economic expansions to continue, albeit, at a slower pace, we have identified five key factors to watch that may play a significant role in what economic scenario unfolds this year.

Business Investment

Since World War II, the difference between average length recoveries and longer ones is largely attributed to late-stage business investment that fuels productivity and gives aging expansions extra legs. If further trade agreement progress is made in early 2020, business confidence may improve more than forecasted, boding well for the economy. However, if political and economic uncertainty escalates, businesses may hold off on new hiring and investments, creating some headwinds to growth.

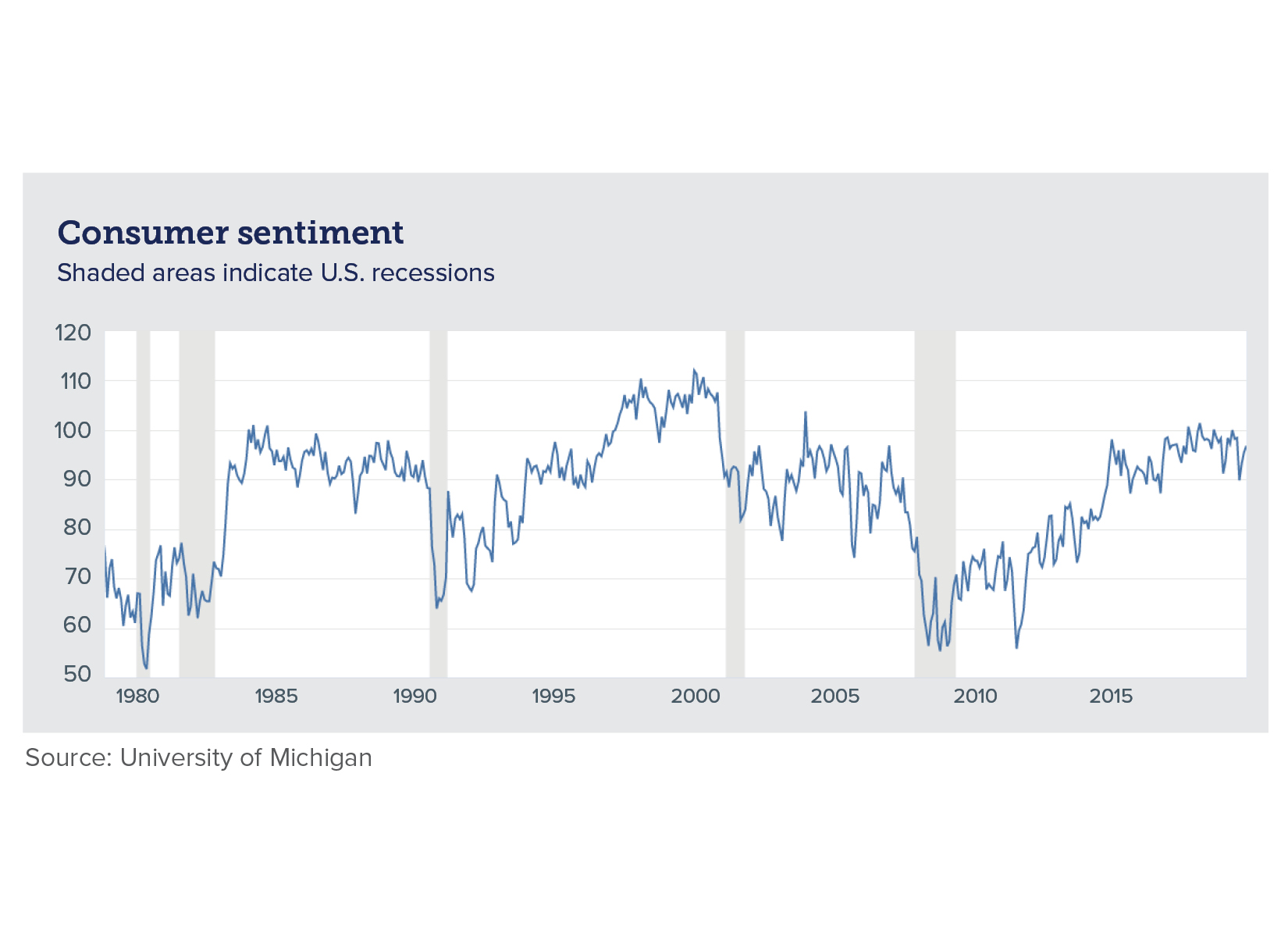

Consumer Confidence

As measured by the University of Michigan Consumer Sentiment Index, consumer confidence remains near its highest level in more than a decade. To keep the U.S. economy moving forward in 2020, households need to keep spending, especially considering a potential slowdown in business investment. Low unemployment and wage growth will be vital components to sustained consumer optimism. We believe the consumer sector is on solid footing, and the risk of a significant drop in consumption remains low.

Global Economy

We anticipate the global economy to remain soft in 2020, although some regions — including certain emerging market economies — are poised for accelerated growth. The Eurozone has essentially exhausted its monetary policy toolkit, as its negative interest rate policy benefits appear to have plateaued. In December of last year, the U.K. finally approved a Brexit deal effective in January. Clarity on Brexit is certainly a positive, but the U.K. has a short transition period of 11 months to agree on their future relationship with the European Union. Besides the continuance of accommodative monetary policies, fiscal stimulus by European and Chinese policymakers may be required to revitalize growth across the globe.

Trade Policies

We entered 2020 with progress being made on trade. The U.S. reached an interim agreement with China in December, and the passage of an amended North American trade pact is anticipated early this year. However, punitive tariffs are still in place between China and the U.S., and it is not clear what will happen next. Markets will likely continue hanging on every word (or Tweet) surrounding trade. We believe this initial progress is merely the beginning of a long cycle of phased-in trade negotiations, and the final terms of the trade agreements should provide much needed clarity for businesses that buy and sell goods and services globally.

U.S. Elections

The upcoming U.S. elections will likely dominate the news in 2020. History suggests President Trump should be favored to win given a strong labor market, higher wages and a good economy. However, these are not normal times — the President’s low approval ratings and impeachment status create a clear opportunity for a Democratic challenger and potential change in control of the Senate. Businesses and investors will be interested in the leading challengers’ proposals on taxation, regulation, trade and healthcare. Although a divided government is the most likely election outcome, the possibility of a single political party controlling the White House, the House of Representatives and the Senate cannot be ruled out.

Markets

Equity and fixed income markets soared higher in 2019, closing out a decade of exceptional market returns. However, investors should reset return expectations for the next decade, anticipate volatility leading up to November’s elections and remain committed to a disciplined investment strategy for reaching their long term goals.

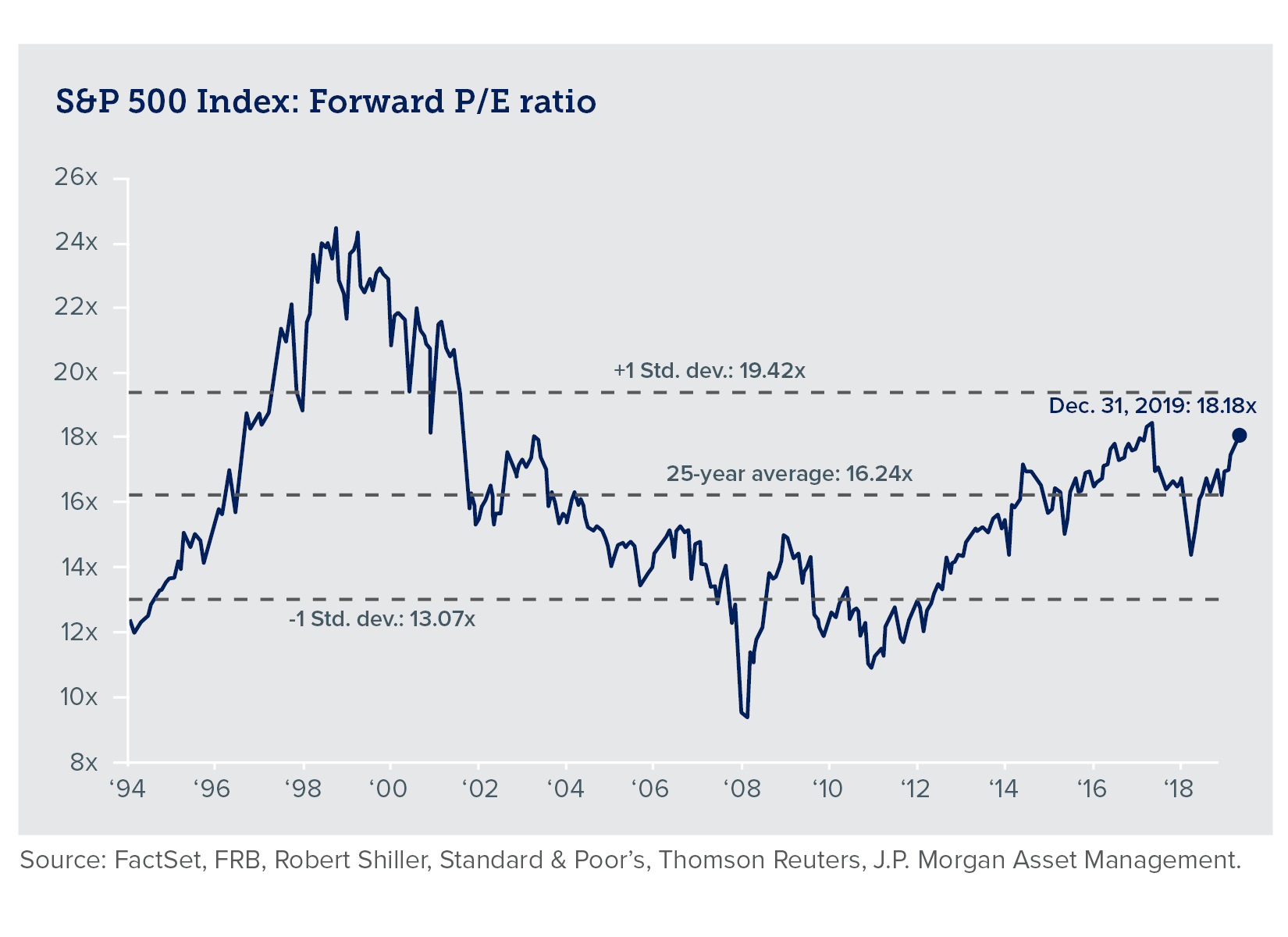

Equities

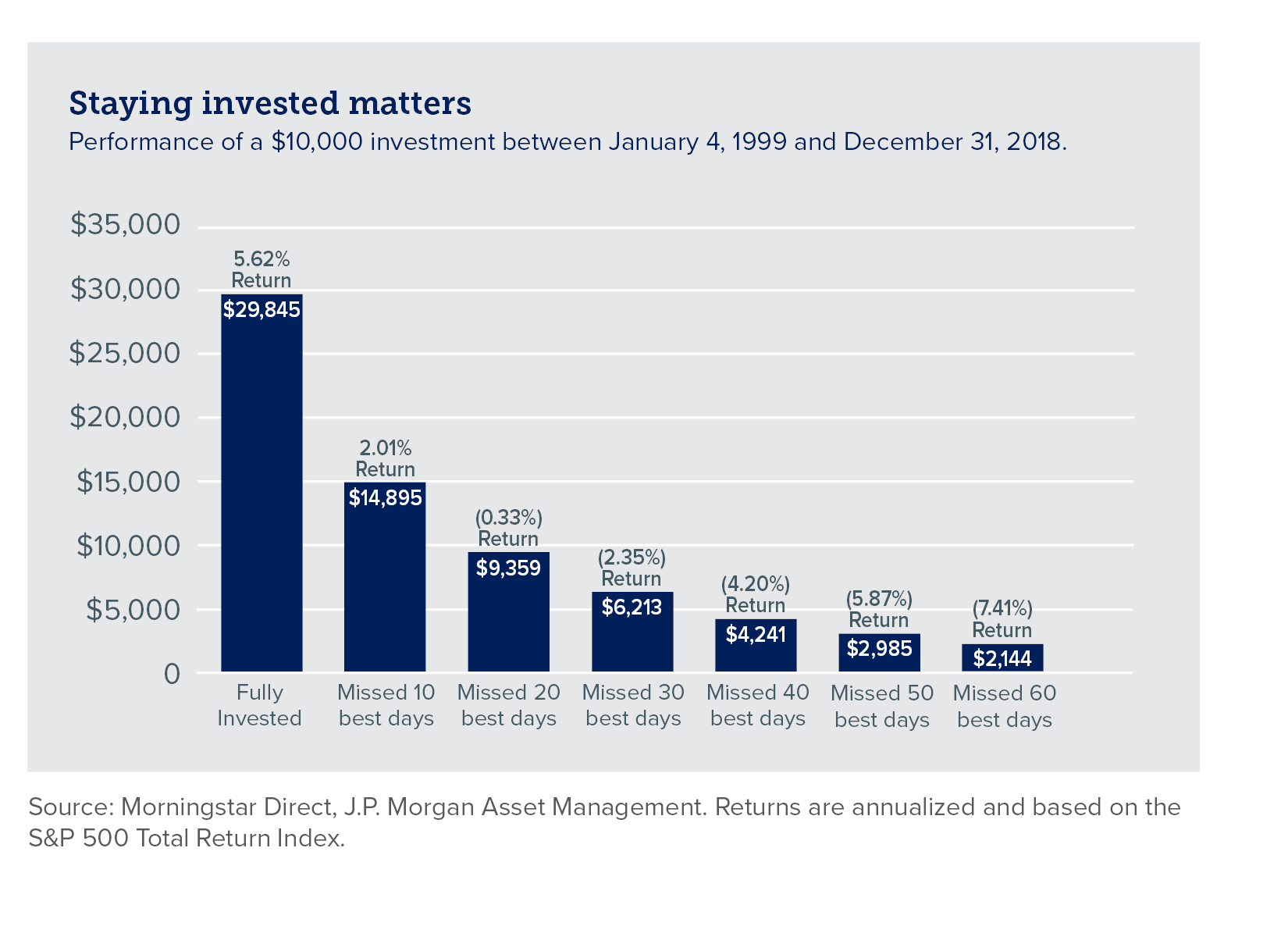

Equity returns are derived from three components: dividend yield, valuation expansion/contraction and growth in corporate earnings. U.S. equities appear fairly valued to moderately expensive based on various valuation metrics. Accordingly, future gains in U.S. equities likely will result in more from their dividend yield and earnings growth than valuation expansion. Based on current valuation metrics, value-oriented stocks appear more attractive than growth stocks, while small cap equities look somewhat more favorable than their large cap counterparts. Although market volatility tends to be higher in an election year, we encourage investors to be well-diversified and avoid letting political opinions influence how they invest.

Our long term return expectations for international equities are higher than that of U.S. stocks because of more reasonable valuations, slightly better earnings prospects and the possible depreciation of the U.S. Dollar. Nevertheless, international equities have ongoing risks such as policy flare-ups, growing government deficits and persistent trade tensions. The higher return outlook for international equities highlights the benefits of global diversification during this period of economic and political uncertainty. We encourage equity investors to evaluate if they are overly concentrated on U.S. equities with little to no exposure to international markets.

Fixed Income

Fixed income markets — including corporate bonds, high yield debt and municipal bonds — experienced strong performance in 2019, although, our near-term and long-term return expectations for fixed income are lower than the exceptional returns posted last year. Still, maintaining exposure to high-quality bonds plays an important role for many investors in reducing risk, increasing portfolio stability and generating income. Rather than viewing bonds as a primary return generating investment, we are encouraging investors to view this asset class as a means of providing balance to portfolios amid potentially higher equity volatility. Furthermore, as investors continue searching for yield in a low-yield environment, they should be aware that higher-yielding instruments generally come with more risk. We believe fixed income investors should focus on quality and diversification rather than chasing yields, including maintaining exposure to U.S. Treasuries, municipal securities (for taxable accounts) and high-quality corporate bonds — especially at this stage in the economic cycle.

Portfolio Considerations

Although the U.S. economy is shifting into a lower gear, the risk of recession in 2020 remains relatively low — there appear to be few signs of large financial imbalances or excessive inflation that often characterize the end of an expansion. However, the odds of encountering a market pullback or recession increase each year this expansion continues. Given these perspectives, we believe investors must have a current financial plan — one that accounts for an investor’s goals, risk appetite and financial capacity. Such plans can help prevent investors from overreacting to near-term market volatility and hurting their chances of meeting their financial goals.

We believe smart investors are likely to be rewarded over the long term. Maintaining discipline, appropriately diversifying portfolios and being patient are key factors in achieving this outcome. Furthermore, we believe it is vital for investors to adhere to time-tested principles, such as long-term focus, active tax management, disciplined asset allocation and periodic portfolio re-balancing in pursuit of their financial goals.

The INTRUST 2020 Economic Outlook is the consensus of the INTRUST Bank, N.A. ("INTRUST") Investment Strategy team and is based on third party sources believed to be reliable. INTRUST has relied upon and assumed, without independent verification, the accuracy and completeness of this third party information. INTRUST makes no warranties with regard to the information or results obtained by its use and disclaims any and all liability arising out of the use of, or reliance on the information. The information presented has been prepared for informational purposes only. It should not be relied upon as a recommendation to buy or sell securities or to participate in any investment strategy. The forward-looking perspectives are not intended to, and should not, form a primary basis for any investment decisions. This information should not be construed as investment, legal, tax or accounting advice. Past performance is no guarantee of future results.

| Not FDIC Insured | No Bank Guarantee | May Lose Value |

Posted:

01/14/2020

Category:

Recommended Articles