Creating an estate plan can feel easier once you understand what it is and how to gather the information you’ll need. An estate plan is a collection of documents that detail the way you want your assets and personal property to be transferred and distributed after you die. It can also include documentation on who should care for your children if they are still minors, as well as your health care directives if you are severely injured or become terminally ill.

Key estate planning documents

- Will

- Power of attorney

- Health care directive

- Beneficiary designations

- Trusts

Do I need an estate plan?

Yes, an estate plan can be helpful for most people who have assets (such as a car, home, home goods, bank accounts, and investments) and a family. It isn’t solely for older adults. Documenting your wishes as an adult of any age can help your family make tough decisions and avoid disagreements that could occur when trying to guess what you would have wanted.

What documents should I include in my estate plan?

The contents of your estate plan will depend on your finances and family dynamics. Importantly, you don’t have to go it alone. A variety of professionals can guide you in creating your plan, including your financial advisor, attorney, accountant, insurance agent, and even your health care provider. If you need a recommendation on where to begin or recommendations for an attorney who specializes in estate planning, your financial advisor is a good place to start.

In general, the following documents will likely be the bulk of your estate plan.

Will

A will, or last will and testament, is a legal document that details how you want your assets and property titled in your name to be distributed after your death. In a will, you can:

- Choose beneficiaries for your possessions.

- Name an executor to oversee the distribution process.

- Appoint guardians for minor children and pets.

- Include instructions for the payment of debts and taxes.

- Outline funeral arrangements.

To make a will, we recommend hiring an estate planning attorney. They’ll ensure you document everything appropriately so that it’s legally binding and your family is able to easily handle your affairs.

Power of attorney (POA)

A power of attorney is a legal document that allows you to give someone you trust (also called “the agent”) the authority to act on your behalf in various matters, both temporarily and if you become physically or mentally incapacitated. The scope of this authority can range from making financial decisions to handling medical care and personal affairs.

You should establish a POA when you are healthy and mentally competent. You’ll want to choose a trustworthy and competent individual as your agent, as they will have significant control over your affairs. An estate planning attorney can walk you through POA scenarios and ensure they’re drafted correctly and meet your specific needs.

- General POA gives broad authority to someone so they can handle your legal and financial matters for a specific period or until you revoke it.

- Ideal for temporary situations, such as when you’re traveling or temporarily unavailable to manage your affairs.

- Durable POA grants someone broad authority to act on your behalf in various matters if you become physically or mentally incapacitated.

- Beneficial for long-term situations where ongoing oversight and decision-making will be needed.

- Helps ensure that important financial, legal, medical, and personal decisions will be consistently managed without interruption.

- Limited POA grants someone the authority to handle specific tasks on your behalf, such as signing documents, managing real estate transactions, or handling a specific financial matter while you are unavailable.

- Ideal for scenarios where you anticipate being absent or busy for a short period.

- Helps ensure that certain responsibilities are taken care of without having to grant the broad, overarching authority of general and durable POAs.

- Allows you to maintain control over more personal or extensive affairs while delegating limited authority to a trusted individual.

- Medical or health care POA allows you to appoint someone to make health care decisions on your behalf should you become unable to do so yourself. (You’ll want to include your medical POA in your health care directive, which we’ll cover in the section below.) The person you choose will:

- Make decisions on medical treatments, surgical procedures, and other aspects of your medical care.

- Consult with your health care providers, review your medical records, and make decisions that align with your wishes and best interests.

Health care directive

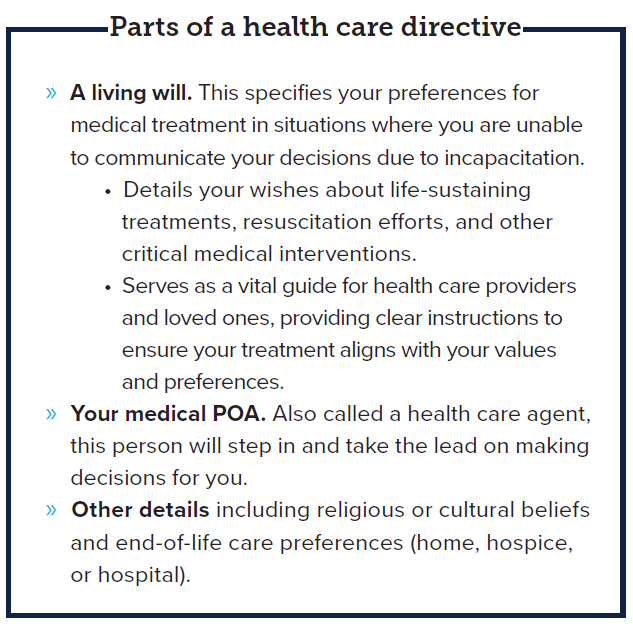

A health care directive is a collection of documents that outline your preferences for medical treatment and end-of-life care if you become unable to communicate your wishes yourself. Offering clear guidance to your health care providers and your loved ones can prevent confusion and conflicts during difficult times.

An estate planning attorney can assist you in drafting a health care directive that accurately reflects your wishes and complies with relevant laws. It’s also a good idea to review your health care directive with your doctor and request they put it in your file.

Beneficiary designations

Beneficiary designations specify who will receive your assets such as life insurance policies, retirement accounts, and other financial accounts when you die.

You’ve likely named beneficiaries already on most of your accounts, but it’s important to double-check with your insurance and financial providers and keep hard copies of your beneficiary designations in your estate plan.

- These designations take precedence over instructions left in a will or trust, so it’s crucial to keep them updated.

- Helps streamline the process of asset distribution by bypassing probate and provides a clear path for your loved ones, minimizing potential conflicts or delays.

What is probate? Probate is a legal process where a court oversees the distribution of a deceased person’s assets titled in the person’s name. Not every estate goes through probate. It can depend on the size of the estate and state laws. But one way to ensure parts of your estate — your insurance and financial accounts — do not end up in probate is to have the paperwork for beneficiary designations properly completed. |

Trusts

Trusts are legal arrangements where one party (the trustee) holds and manages assets for the benefit of another party (the beneficiary).

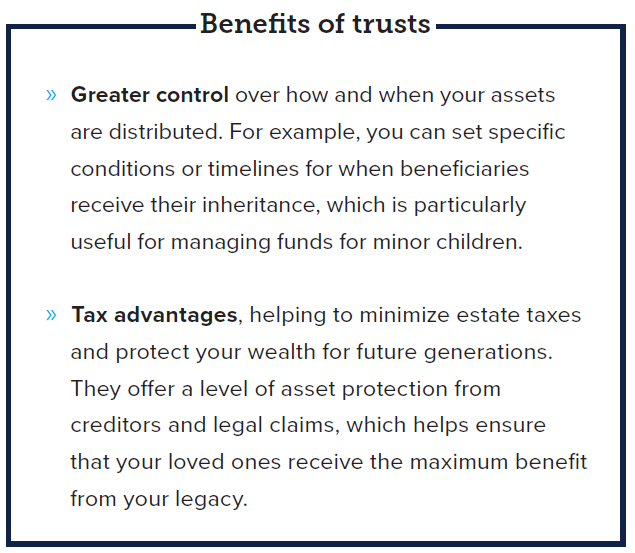

Trusts aren’t necessary for every estate plan, and you can talk with your financial advisor about whether it’s a good choice for you. Trusts do, however, offer various benefits that go beyond what a simple will can provide.

One of the primary advantages of a trust is the ability to avoid probate, which can be a lengthy and costly process.

By placing assets in a trust, they can be transferred to beneficiaries without the need for court involvement, ensuring a quicker and more private distribution. This can be especially beneficial for estates with significant assets or complex family situations.

At INTRUST Bank, we manage various trusts — some that are multi-generational. We can serve as successor trustee or co-trustee to help your legacy endure, including management of your charitable giving.

Where should I keep my estate plan? Consider storing your estate plan in a fireproof and waterproof safe to protect it from any potential damage. You can also keep digital copies in a secure, encrypted cloud storage service as a backup. Make sure to:

Why estate planning matters An estate plan is a key piece of your financial strategy. It ensures that your assets are distributed accordingly, and your medical care is handled as you wish, all while protecting your loved ones from potential legal and financial complications. By thoughtfully preparing and managing your estate plan, you can provide peace of mind, preserve your wealth, and create a legacy that reflects your values and priorities. Whether through wills, trusts, or beneficiary designations, an organized and comprehensive plan now can make all the difference for your family’s future. |

The information is general in nature and is not intended to be, and should not be construed as, legal or tax advice. In addition, the information is subject to change and although based upon information that INTRUST considers reliable, is not guaranteed as to accuracy or completeness. INTRUST makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. Past performance is no guarantee of future results.

| Not FDIC Insured | No Bank Guarantee | May Lose Value |

Posted:

06/04/2025

Category:

Related Blog Posts