Theme

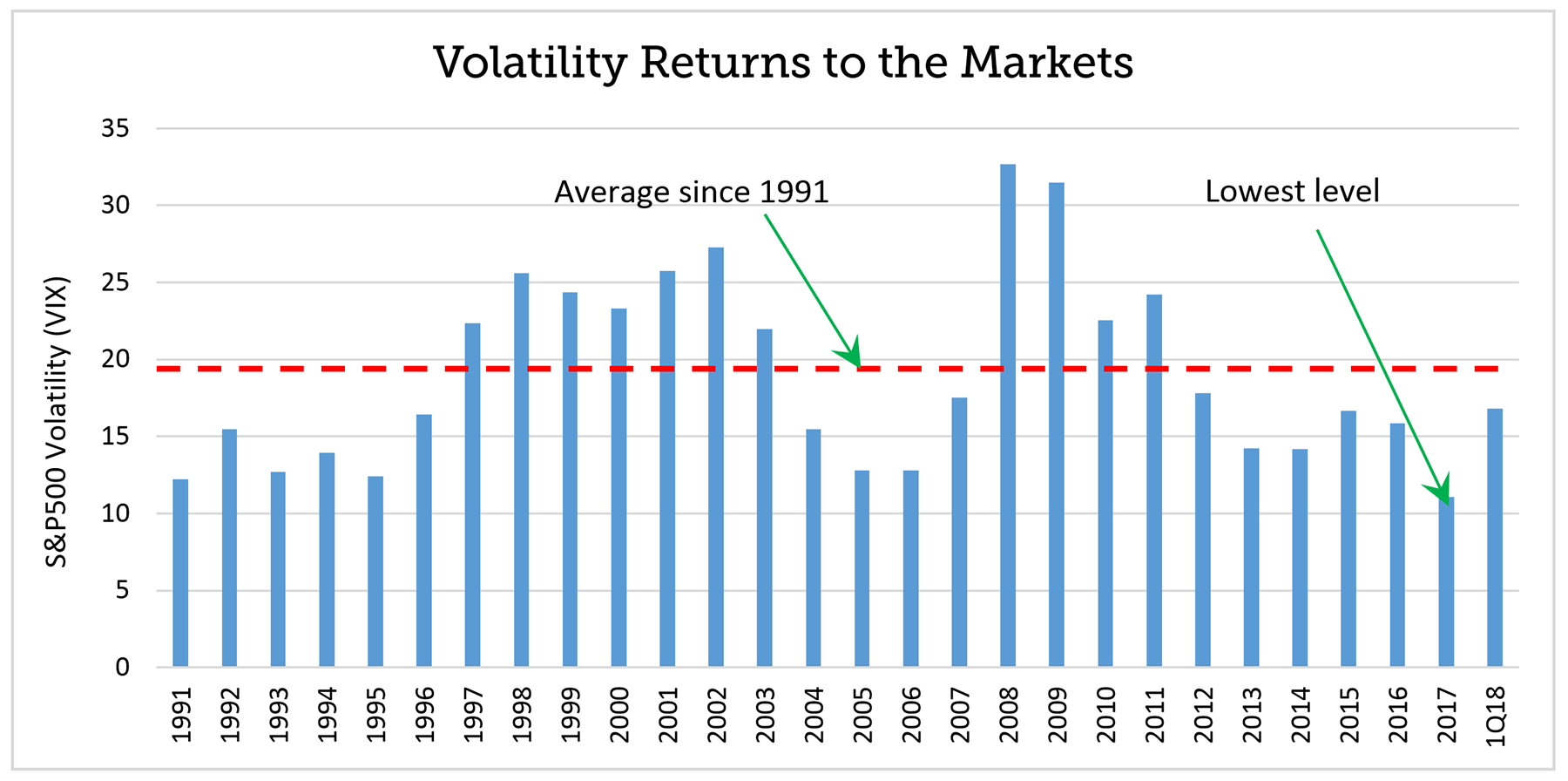

On the heels of a historically quiet year in the markets, volatility appears to be returning to normal levels.

Drivers

Likely drivers to increase market volatility include:

- Inflation Fears — Low unemployment, increased wage pressure and consumer spending, and proposed trade barriers are driving nervousness of an accelerating pace of inflation

- Trade Concerns — Protectionist rhetoric is leading to talks of Trade Wars among key US trading partners (most notably China) and fueling uncertainty in the markets

What does this mean for you?

Discuss your long term goals and sensitivity to risk with your INTRUST Wealth Team.

- Tax–Efficient Investing — During higher market volatility, improve your after–tax portfolio performance through capturing any tax losses.

- Get Risk Right — After a quiet year in the markets, ensure you allocate your portfolio with long-term risk tolerance in mind.

Forward-Looking Perspectives

Economy

- The economic expansion showed continued strength as the US GDP grew in the 4th quarter of 2017 at a 2.5% annualized rate. If the current expansion continues, in June 2018 it will become the second longest since WWII and will become the longest in June 2019.

- Core inflation remains muted below the 2% Fed target but increases may result from potential trade tariffs on imported goods.

- GDP growth should moderate due to tightened credit standards and a less accommodative monetary environment, indicative of a late-stage business cycle.

Equity

- Market volatility rose significantly during the first quarter – returning to more historical levels – as global equity markets corrected from all-time highs.

- Tax reform and favorable administrative policies should continue to fuel earnings growth, providing a foundation for tailwinds for equity markets.

- Developed and Emerging Markets continue to enjoy economic expansion but could be hampered by protectionist US trade policies.

Fixed Income

- The much-anticipated Fed rate increase in March will likely put pressure on short-term rates and lend further concern to the flattening yield curve as short-term rates rise faster than the long-term rates. Current projections call for another two to three Federal rate hikes in 2018.

- Long-term US bond yields will continue to be pressured by high demand from the yield-starved global bond market.

- Prudent investors should avoid the temptation to reach for yield by positioning portfolios with shorter maturities and higher quality, emphasizing total return over yield.

Alternatives

- As volatility returns to more normalized levels (as denoted by the Chicago Board Options Exchange’s Volatility Index “VIX”) Alternative Investments may play an increasingly important role in supporting a diversified source of returns and risk exposure.

- Our allocation to Real Asset strategies continues to generate positive performance and protect portfolios against rising inflation; with the potential for higher inflation, Real Asset strategies may continue to experience upward momentum.

The INTRUST Market Perspectives are the consensus of the INTRUST Bank, N.A. ("INTRUST") Wealth Investment Strategy team and are based on third party sources believed to be reliable. INTRUST has relied upon and assumed, without independent verification, the accuracy and completeness of this third party information.

INTRUST makes no warranties with regard to the information or results obtained by its use and disclaims any and all liability arising out of the use of, or reliance on the information.

The information presented has been prepared for informational purposes only. It should not be relied upon as a recommendation to buy or sell securities or to participate in any investment strategy. The Forward–Looking Perspectives are not intended to, and should not, form a primary basis for any investment decisions. This information should not be construed as investment, legal, tax or accounting advice. Past performance is no guarantee of future results.

| Not FDIC Insured | No Bank Guarantee | May Lose Value |

Posted:

05/20/2019

Category:

Recommended Articles