Economic Impact of COVID-19

In January, the U.S. economy appeared healthy. Unemployment was low. Consumers were confident. Growth prospects remained positive for the foreseeable future. However, the 12-year U.S. economic expansion came to an abrupt halt in March, as effects of COVID-19 reverberated around the globe and across our nation. Now, recession in 2020 seems all but inevitable.

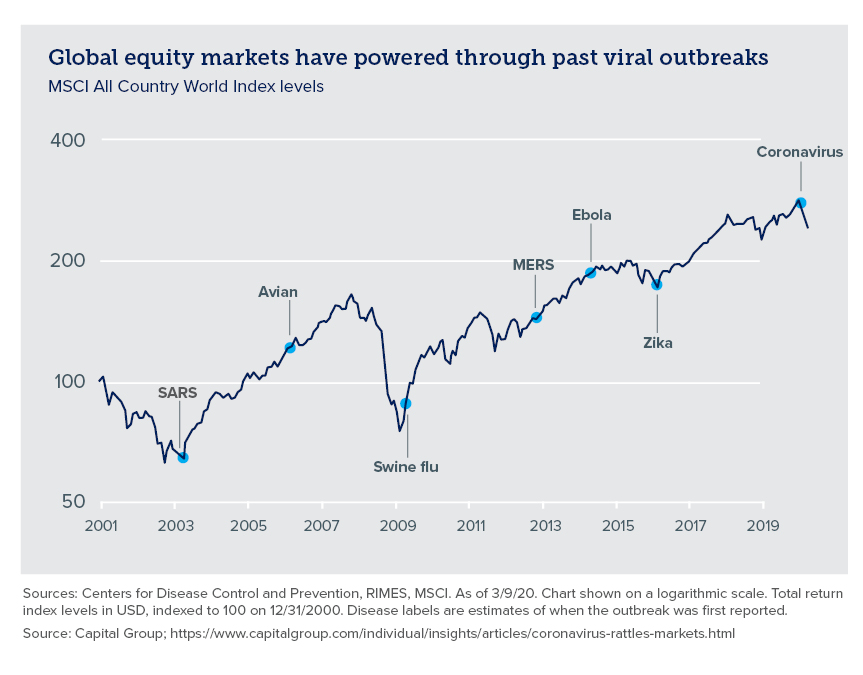

History informs us that, like most geopolitical events, pandemics and the resulting economic impacts are relatively short-lived. Nevertheless, the timing of economic recovery remains uncertain. If the U.S. begins to revert back to normalcy later this year, the slowdown should be relatively short-lived. But if stopping the virus takes longer, economic recovery may take longer.

Best Defense: Making a Plan and Sticking to it

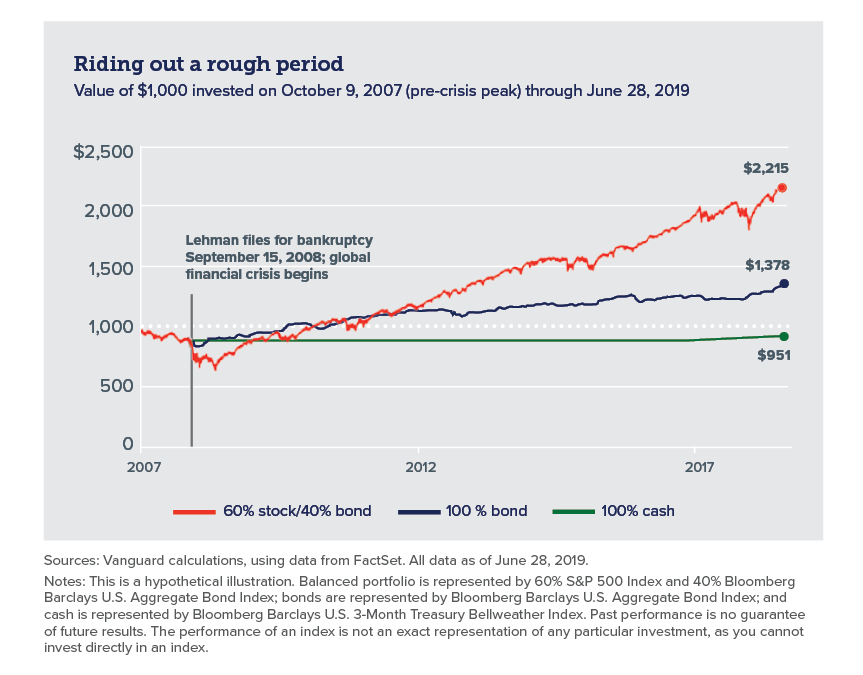

Financial planning is the cornerstone of INTRUST's advisory services. A goals-based financial plan prepares you and your portfolio for financial system shocks, whenever they happen to occur, and helps focus on the factors of your investing strategy we can control (including things such as asset allocation and tax costs). Given the current environment, we are encouraging clients with financial plans to let us update them with you. In doing so, we are able to more precisely assess the impact of the market selloff relative to your future needs, wants and wishes. For clients without a detailed financial plan, we are encouraging them to collaborate with us to develop one.

Bearish market conditions — while inevitable — don't last forever. As a savvy investor, you can ignore short-term pullbacks of the market (and any commentary that might cause you to veer off course) and remain committed to achieving your long-term vision. Downturns come and go. The results of a well-designed and faithfully followed plan, on the other hand, can serve you the rest of your life.

U.S. & Regional Economy

- Leaders across the U.S. are trying to reduce the growth rate of COVID-19's spread through social distancing, travel restrictions and "stay-at-home" orders, but these efforts also are leading the U.S. into a recession.

- Driven by recessionary concerns, the Fed lowered rates to near zero in two emergency cuts in March and restarted quantitative easing.

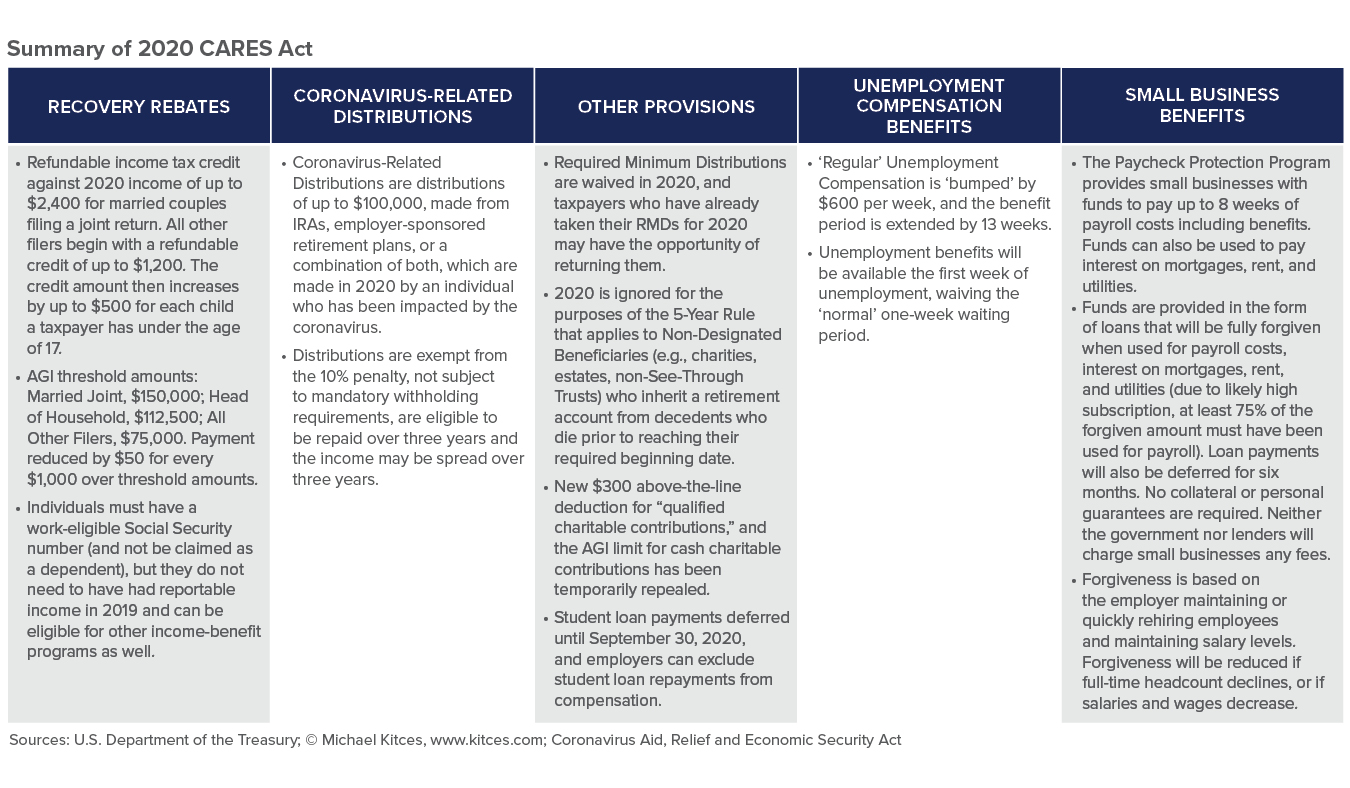

- The Coronavirus Aid, Relief and Economic Security Act (CARES) was signed into law on March 27, a $2+ trillion stimulus package offering loan guarantees, bailouts, generous unemployment benefits and cash payments to U.S. households.

- A Saudi-Russian oil price war broke out, sending oil prices to an 18-year low during the first quarter.

- Kansas Governor Laura Kelly announced a "stay-at-home" order for all of Kansas, beginning on March 30.

- Oklahoma Governor Kevin Stitt ordered all nonessential businesses in Oklahoma to close April 1, and extended 'Safer at Home' orders for those 65 and older and with compromised immune systems.

- The unemployment rate is anticipated to quickly escalate, potentially climbing to double digits in the second quarter.

- More than 55,000 Kansans and nearly 45,000 Oklahomans filed initial unemployment claims in the week ending March 28.

Growth Assets

- A sharp selloff in growth assets placed equity returns in bear market territory for the first time in 11 years.

- Market volatility soared in March, with swings of 5%+ becoming commonplace during the month.

- Corporate earnings are coming under pressure from the business disruption caused by the coronavirus concerns.

- Recent Fed action and fiscal stimulus may help stabilize equity markets.

- The U.S. equity market appears cheaper than it did a month ago, as the S&P 500 Index's price-to-earnings ratio (a measure of the market's valuation) is currently lower than it has been for quite some time.

- As corporate earnings retreat from the economic slowdown, the stock market many continue experiencing heightened levels of volatility.

Defensive Assets

- Treasury rates have fallen sharply with the 10-year Treasury yield dropping below 1%.

- Corporate and high-yield bonds have seen spreads widen relative to Treasury yields, but have provided better downside protection than equities during the recent market selloff.

- The drop in yields have helped to buoy prices of high quality bonds during the first quarter.

- An environment of higher levels of interest rate volatility is likely to continue, particularly given the economic uncertainty and the upcoming 2020 U.S. elections.

The INTRUST Quarterly Perspectives are the consensus of the INTRUST Investment Strategy team and are based on third party sources believed to be reliable. INTRUST has relied upon and assumed, without independent verification, the accuracy and completeness of this third party information.

INTRUST makes no warranties with regard to the information or results obtained by its use and disclaims any and all liability arising out of the use of, or reliance on, the information.

The information presented has been prepared for informational purposes only. It should not be relied upon as a recommendation to buy or sell securities or to participate in any investment strategy. The Forward–Looking Perspectives are not intended to, and should not, form a primary basis for any investment decisions. This information should not be construed as investment, legal, tax or accounting advice. Past performance is no guarantee of future results.

| Not FDIC Insured | No Bank Guarantee | May Lose Value |

Posted:

04/10/2020

Category:

Recommended Articles