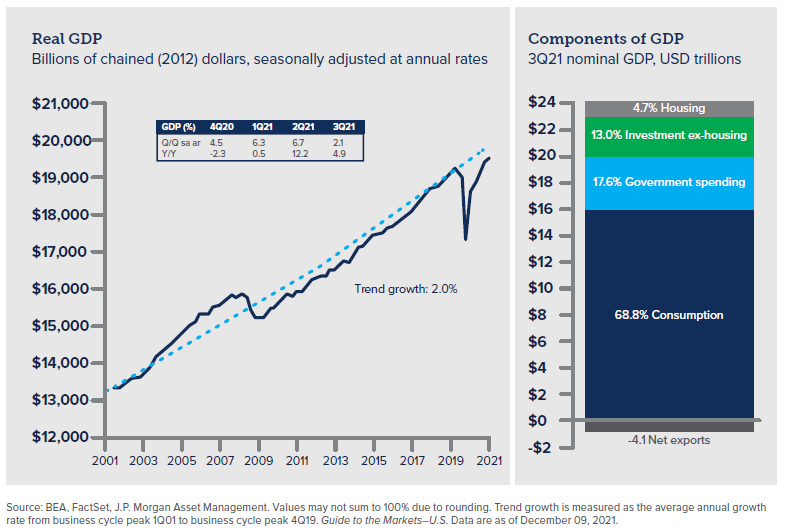

Global economic growth over the past two years largely has been affected by the mandated shutdowns and fiscal stimulus in response to the COVID-19 pandemic. The 2020 recession, which turned out to be the deepest but shortest of all recessions in the post-World War II years, was met with substantial fiscal relief and recovery legislation, together with a highly accommodative monetary policy that allowed the economy to recover. About half of the economic losses incurred in the recession recovered relatively quickly, but subsequent waves of the virus have contributed to an uneven pattern of GDP and employment growth in the post-2020-recession recovery and expansion.

As the U.S. economy continues to recover in 2022, it faces headwinds of labor shortages, supply chain disruptions, and higher inflation. In the following pages, we evaluate the current economic environment and its implications for businesses and investors.

U.S. Economy

Uneven Economic Growth

In our 2021 INTRUST Economic Outlook, we outlined three potential paths for the U.S. economic recovery following the shutdowns in 2020 due to COVID-19. By most measures, the actual recovery path we experienced in 2021 exceeded our most optimistic forecast. This year we look at a base case for continued economic growth in 2022, along with conditions which might cause growth to differ from those expectations.

We expect global economic recovery to continue through 2022, albeit at a reduced and uneven rate. Reduction in fiscal and monetary stimulus should cause economic growth rates to moderate. With the fastest pace of the recovery now behind us, further economic growth likely will be fueled by strong pent-up consumer demand for goods and services and inventory rebuilding.

Many of the key factors that will likely determine the growth of the U.S. economy in 2022 are interrelated. Our base case scenario suggests the U.S. economy will expand in the 3% - 4% range in 2022. This scenario assumes:

- Many of the supply chain disruptive issues will slowly be resolved throughout the year.

- The Federal Reserve (“Fed”) will reduce the accommodative policies put in place to support the initial economic recovery. Subsequently we expect the Fed to tap the brakes on the U.S. economy by raising rates.

- Large-scale business interruptions in response to current and future COVID-19 variants will be muted as medical advancements continue and business contingency plans counter short- and long-term exposure impacts.

There are several factors which could have significant positive or negative effects on our base growth outlook. We discuss these below in more detail.

Labor

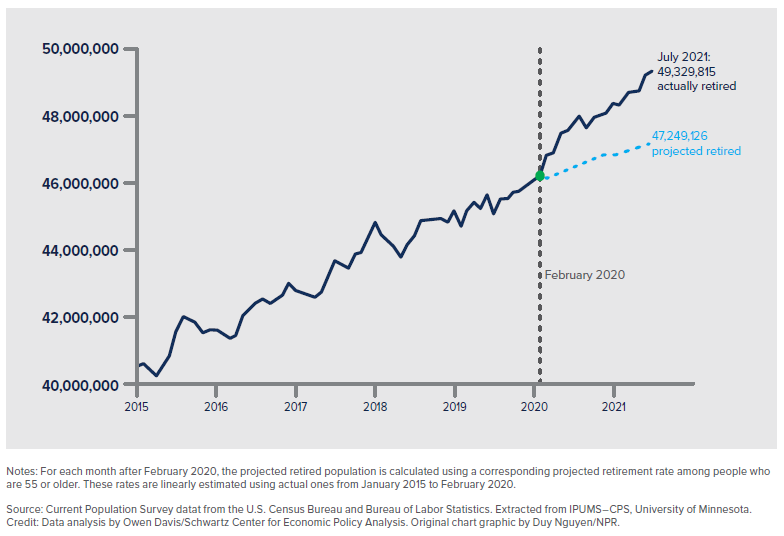

Perhaps the biggest surprise of this economic recovery has been the pronounced shortage of labor. Largely in reaction to the COVID-19 virus and its many ramifications, the U.S. labor force is experiencing a tsunami of changes in employment behavior. A surge in retirements occurred as an estimated 2 million extra people left the U.S. workforce in 2021. Improved personal balance sheets, concern over COVID-19 exposure, and changes in workplace policies motivated a large portion of the population to retire.

Employees are also rapidly resigning from their current jobs as higher pay, flexibility, and their inner entrepreneurial spirit are luring them away. The result is that labor demand currently exceeds supply. Labor likely will be a chokepoint for GDP growth in 2022 as the U.S. economy and several global economies quickly approach full employment.

Efforts to increase worker productivity should intensify as businesses seek to provide goods and services with fewer employees. At a basic level, GDP is the product of the number of workers multiplied by their productivity. Thus, with fewer employees in the workforce, productivity must increase to grow the economy. Wage growth pressures will likely persist through 2022 as employers compete for labor, resulting in higher base wages and producing longer-term inflationary pressures. The competition to recruit and retain talent has heightened as prospective employees seek increased flexibility and enhanced benefits.

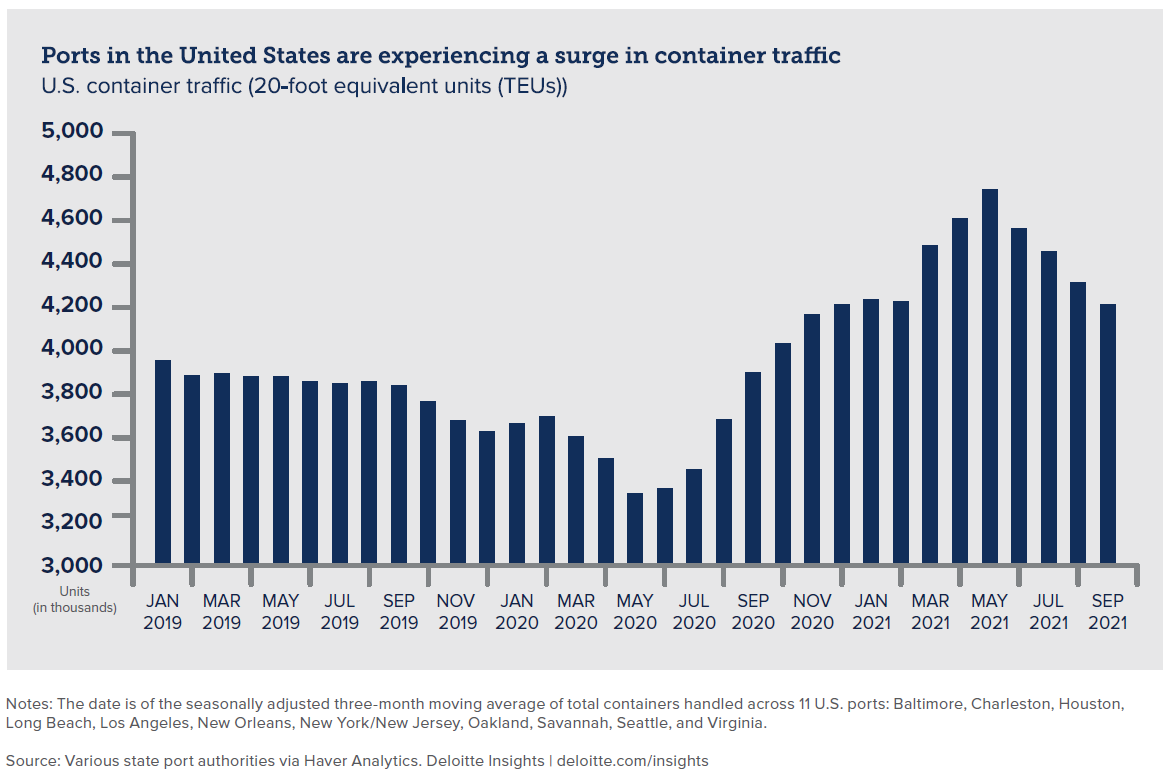

Supply Chain

As global economies recover, disruptions in the supply chain continue. Complex global supply chains could not quickly respond to the closing and restart of an entire economy. In addition, pent-up demand for durable goods and widespread labor shortages have been key contributors to these supply chain disruptions. In light of this, there appears to be a measurable transition towards deglobalization as businesses seek greater control over the supply of intermediary products/services. To that end, competitive low pricing (which may assist with tempering longer-term inflation) will be imperative to net export economies as they seek to retain market share.

In the short-term, however, onshoring and increased slack in supply chains will likely create inflationary pressures due to wage differentials, but these will be offset to a degree by transportation costs, which have increased significantly during the pandemic. Overall, we view supply chain inflationary pressures as likely temporary.

Monetary Policy

The pace at which central banks unwind their accommodative policies will serve as a barometer to gauge economic health. We expect the Fed to implement a more normalized stance to fulfill their dual mandate of low inflation and full employment. Fed actions likely will be measured and largely reactionary to economic data. The risks of taper “missteps” are high as the Fed unwinds monetary policy. However, the Fed is attempting to be quite transparent in their actions in order to mitigate any negative market reactions to its policy changes.

Inflation, which has not been a significant factor for over a decade, could curb consumer activity if it persists. Wage inflation – as opposed to supply chain inflation – will likely be a key factor in central bank actions. Actions of the central banks in the major developed markets will be similar to those taking place in the U.S., with rate increases and a reduction in fiscal stimulus, although the timing and extent of these actions will vary greatly by economy.

Other items of note

In addition to the primary drivers of economic activity for 2022, there are several items which could have a smaller, yet meaningful, impact. Predictions around these lesser drivers are difficult, providing a potential “wild card” impact.

COVID variants

A third strain of the COVID-19 virus is currently affecting the nation. Although future variants of the virus are likely, expanded ability to counter new COVID threats with vaccines and

therapeutics that are becoming increasingly available should mitigate the need to significantly curtail consumer activity. We think the large-scale mandated shutdowns that took place in the early days of the pandemic are unlikely to recur, but vaccine

mandates in areas of the job market that are already struggling for employees could have a negative effect on the workplace and economic growth. An improvement in our overall pandemic posture should provide a significant boost to those areas of the

economy which were negatively impacted the most, such as travel and entertainment.

Mid-term elections

Although U.S. mid-term elections will not take place until November, campaign rhetoric will likely dominate headlines throughout most of the year. The political divide between the

two parties is great, although bi-partisan efforts will become more likely if Republicans regain a majority in either house of Congress. Historically a divided Congress is beneficial to markets, as legislative gridlock precludes the pendulum from

swinging too far in either direction.

Geo-political challenges

Significant geo-political challenges could dominate global headlines in 2022. China and Russia are actively looking to expand their influence and footprint in Europe and Asia.

While military intervention is presently considered unlikely, economic sanctions could further exacerbate supply chain issues and have an inflationary effect. The Mid-East remains unsettled, and issues such as climate change, immigration, and social

justice could impact market performance.

Regional Economies

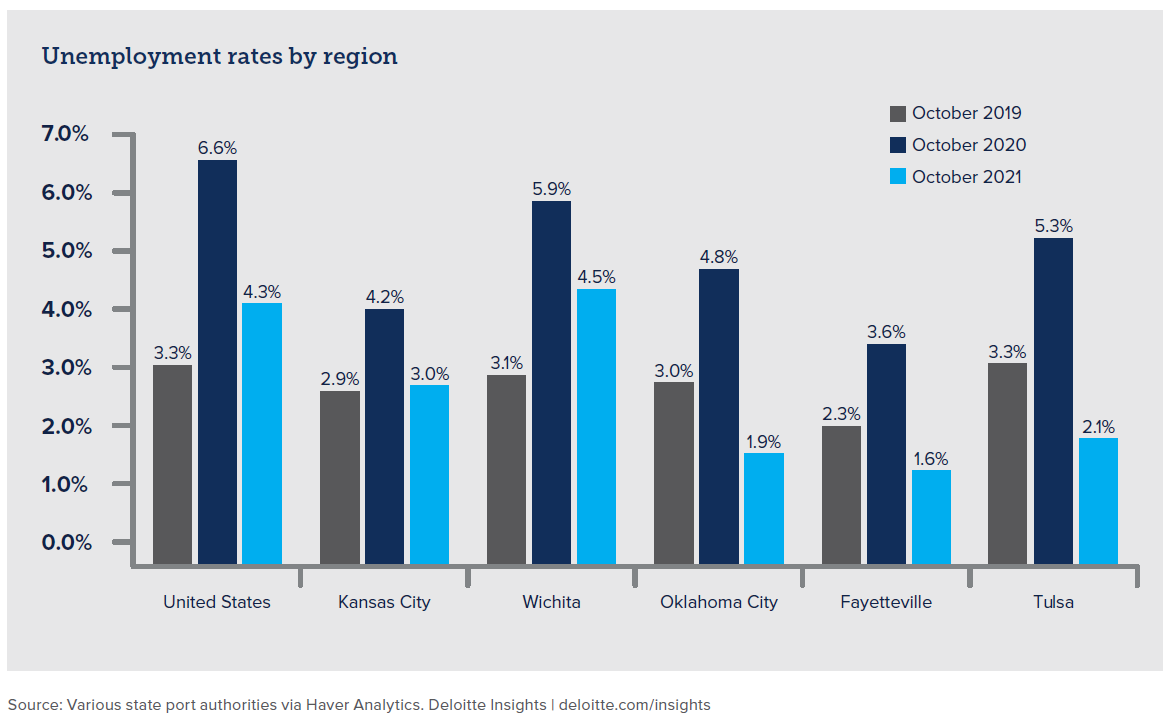

The regional and local economies in Kansas, Oklahoma, and Arkansas experienced strong economic recovery in 2021. Many of the factors that will affect continued recovery on a national level will drive growth at local levels as well. We expect continued growth in Kansas, Oklahoma, and Arkansas through 2022, but to differing degrees.

Northeast Kansas

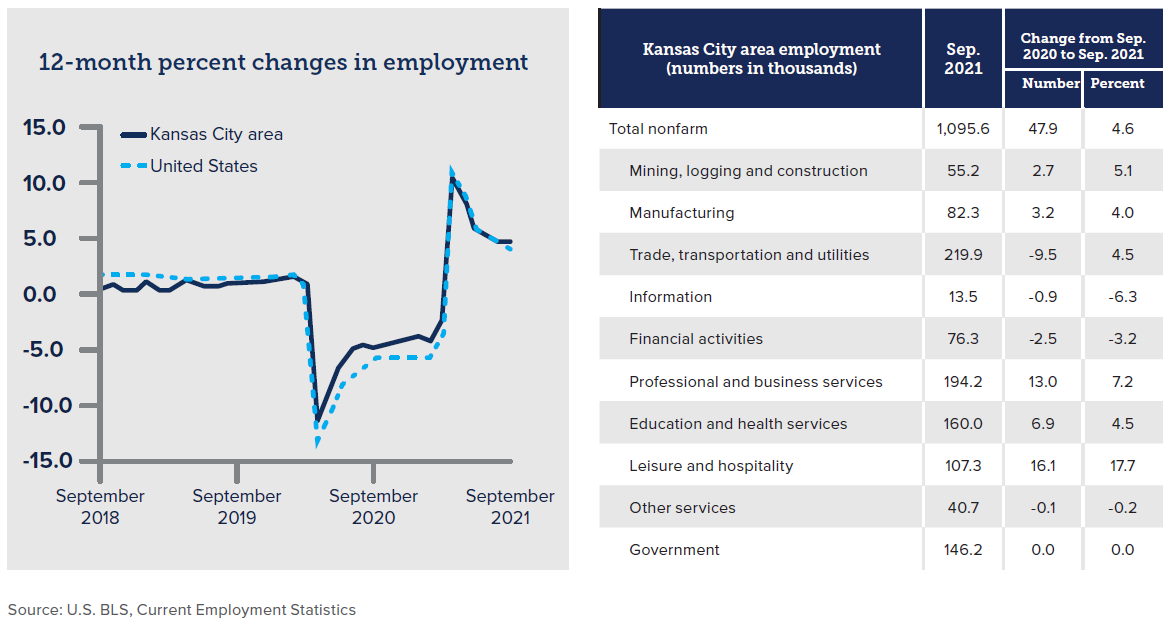

Kansas City: The Kansas City area has a diverse business population that allows the market to weather disruptive economic forces. The area saw steady employment growth in 2021 which should continue through 2022. The professional services labor force (the largest labor segment) has exceeded pre-pandemic levels which will serve as a strong foundation leading into 2022. Strong growth should continue in the real estate sector, particularly in the areas of residential, multi-family, and industrial development. Manufacturing and distribution have experienced good demand for their products and services, but that is impacted by labor and supply shortages.

Kansas City's year-over-year changes in employment on nonfarm payrolls and employment by major industry sector

Lawrence and Topeka: The COVID-19 pandemic created a downturn in the Lawrence and Topeka economies, but the recovery of those lost jobs is well underway. It appears that consumers have resumed their spending plans, which may result in a return to increased hiring in the months ahead. However, with the high demand of employees in almost all sectors, many service industry jobs are going unfilled as small family-owned businesses compete with larger corporations for top talent. Another uncertain headwind for the local Lawrence economy is the downturn in enrollment at the University of Kansas. Providing affordable housing continues to be significant challenges for this region, although Topeka is experiencing an increased housing supply due to reasonable land costs and infrastructure support from the county and city. The Topeka community has strong private/public partnerships in place and increased economic development momentum is seen from the national Plug and Play Entrepreneurship program, downtown investment initiatives, and a focus on the ability to attract and retain talent with financial incentives for living in Topeka.

Manhattan and Junction City: The local economies of Manhattan and Junction City have stabilized from the impact of COVID-19 and more business development is expected in 2022. Kansas State University curtailed many activities last year, but enrollment is rebounding, and activities are trending back to normal, including sporting and community events which are vital for the local economy. Fort Riley continues to be a large economic driver in this region. Local business owners are aggressively looking for employees and expanding their pro-growth attitude for attracting new businesses to the region.

South Central Kansas

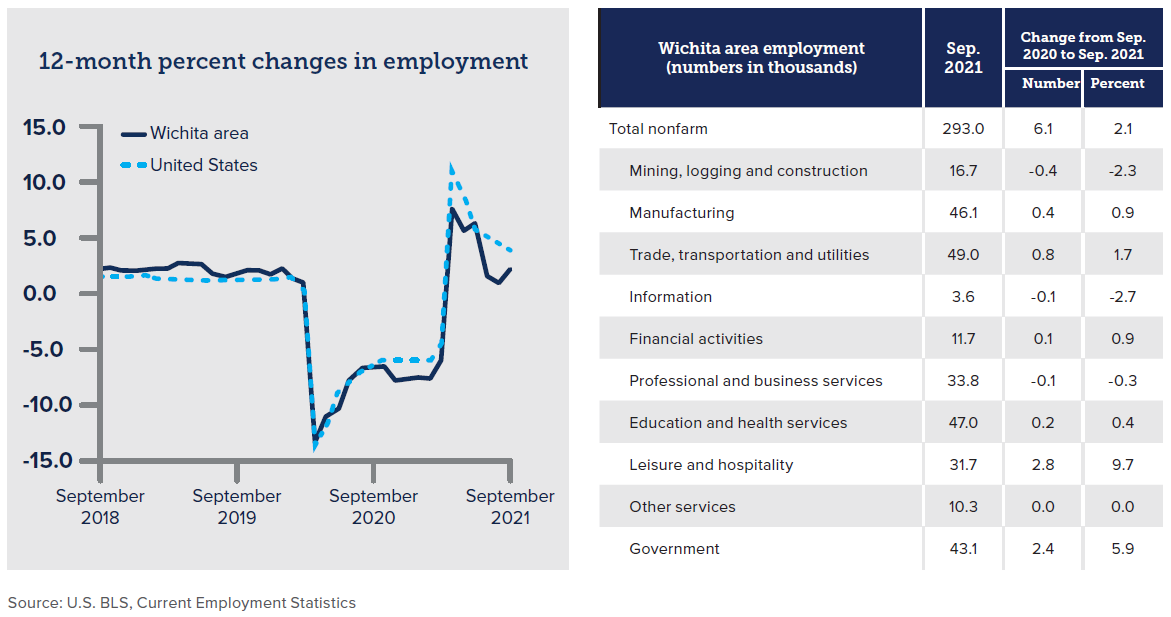

Wichita: Employment in Wichita grew in 2021 but supply chain issues and the continued impact of COVID hampered growth in almost every industry. Construction notably lagged the market at large, as one of the sectors most heavily impacted by supply chain issues. The aircraft industry in Wichita provides both a challenge and an opportunity in 2022. Air travel continues to lag pre-pandemic levels, forcing airlines to manage their cash flows carefully and limit expenditures on new aircraft. Air travel will likely continue to rebound gradually over the course of 2022 which should allow airlines to place much-needed orders for new planes to replace the aging portions of their fleets.

Wichita's year-over-year changes in employment on nonfarm payrolls and employment by major industry sector

Newton and Harvey County: The Harvey County Market employment numbers remain good. Supply chain disruptions and increased prices in raw materials have caused marginal shrinkage in profit margins, particularly in the manufacturing sector. However, aviation production is expected to increase in 2022 and healthcare opportunities will continue to be strong drivers of economic growth. As with the economy nationwide, the pressure to retain employees along with competition for new quality skilled labor will continue to be an ongoing challenge. Agricultural production is a significant component of the Harvey County economy. Weather conditions through the 2021 spring and summer provided better than average harvest yields. Higher commodity prices are helping to offset the challenges presented by increasingly high input costs.

Butler County: Oil and gas production and services, residential construction, and health care are three industries that contribute significantly to the Butler County economy. Recent increases in the price of oil has boosted the energy sector in Butler County. Reductions in oil supply resulted in increased revenues and both local operators and the businesses that support them have benefited. The housing market continues to be strong as local demand exceeds existing inventories and new construction has been hampered by labor shortages. As with other regions, the healthcare industry has experienced strong growth through the pandemic. The shortage of health care workers is an industry-wide challenge. The outlook for 2022 continues to be strong in each of these areas.

Oklahoma

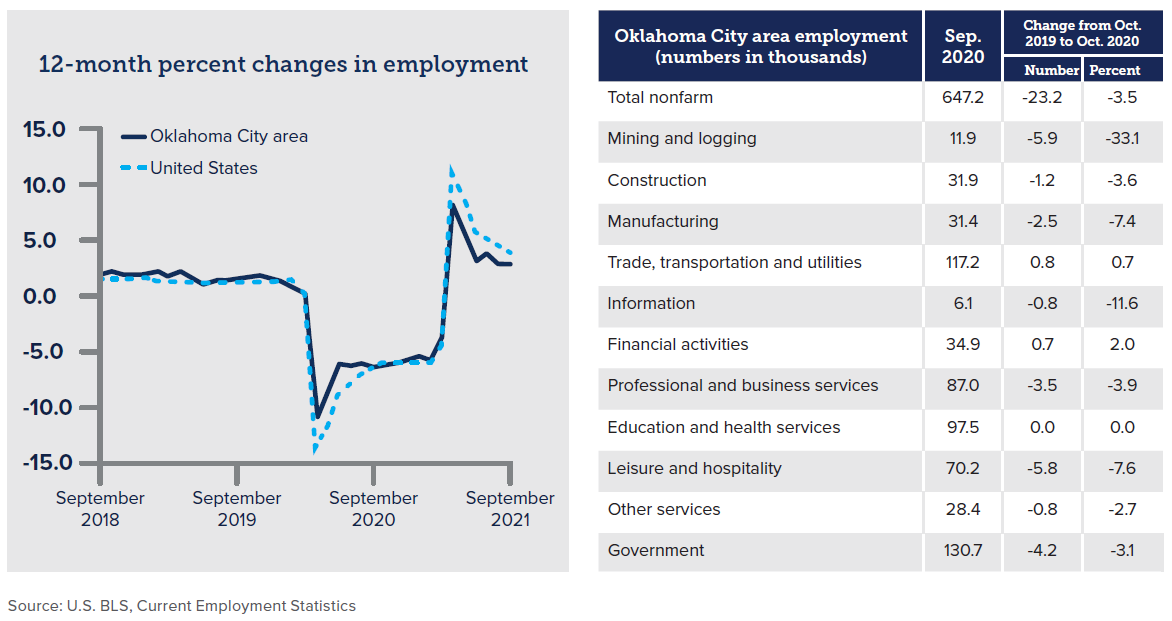

Oklahoma City: Oklahoma has one of the lowest unemployment rates in the country. This represents a significant challenge for the state, as it continues to grow the commercial and military aerospace industry, which is the state’s second largest industry behind oil and gas. The oil and gas industry is experiencing a small boom in activity through further investment in proven, developed and producing oil and gas fields. Continued growth in the oil and gas and aerospace industries provide the greatest opportunities for the region. In addition to the production and manufacturing industries, residential construction continues to be robust across the state with buyers attracted by both low interest rates and Oklahoma’s low cost of living. As with many other markets, Oklahoma City’s principal challenges center around the quantity and quality of its workforce and the supply chain issues affecting a number of industries.

OKC's year-over-year changes in employment on nonfarm payrolls and employment by major industry sector

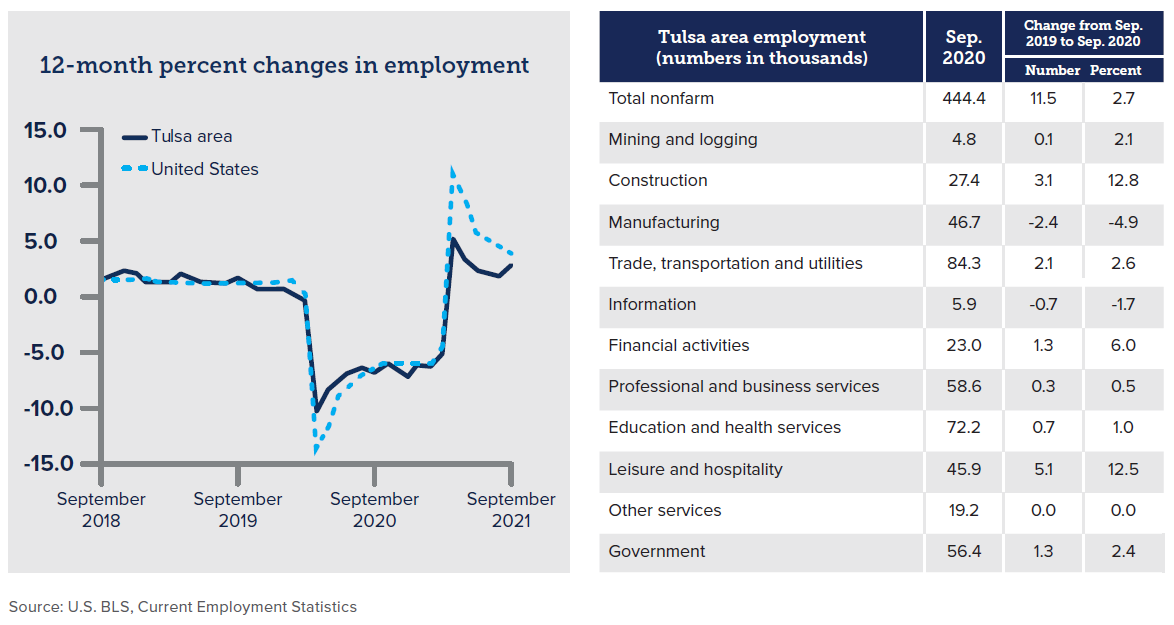

Tulsa: The Tulsa economy has stabilized from last year, buoyed by increased activity in energy, health services, and logistics. Strong commodity prices have helped the energy sector to rebound from both a production and employment perspective. The area is also heavily influenced by the transportation and logistics sectors, with new fulfillment centers for Amazon, Macy’s and Wal-Mart, as well as increased activity at the Port of Catoosa on the Arkansas River. As with other economies, labor supply will weigh on continued growth in 2022 as the area nears full employment and competition for skilled labor increases.

Tulsa's year-over-year changes in employment on nonfarm payrolls and employment by major industry sector

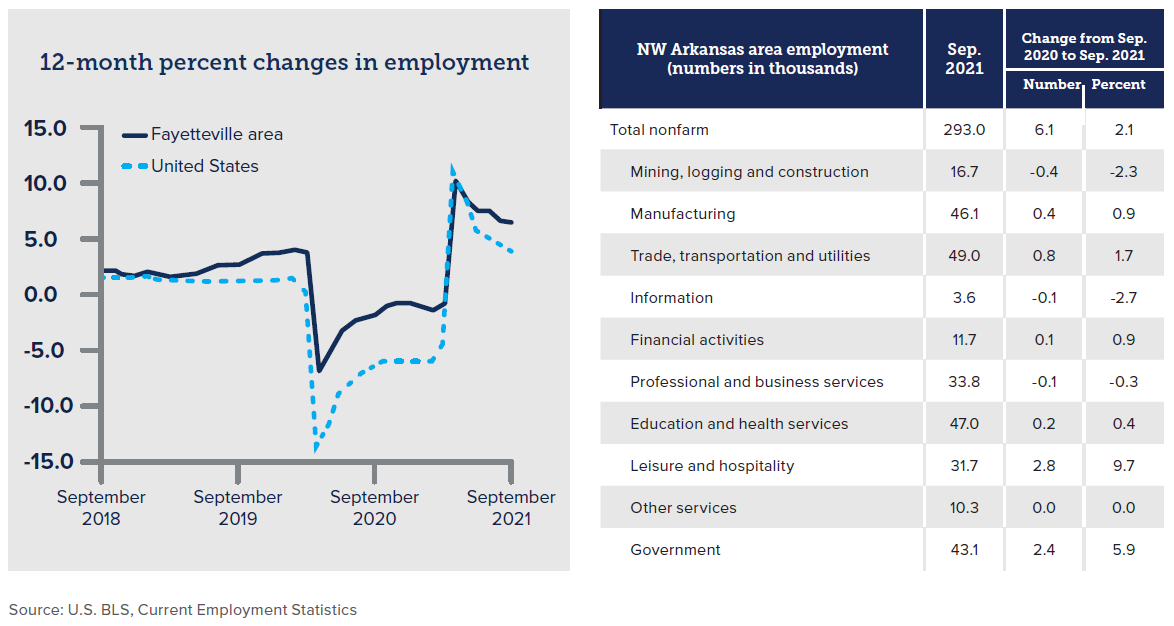

Northwest Arkansas

Economic activity in Northwest Arkansas (NWA) has been exceptionally strong through the recovery with many metrics exceeding pre-pandemic levels. Business starts continue at a significant pace, and sales tax revenue is up significantly in 2021. The region continues to experience a high influx of new residents, resulting in increasing consumer spending. A business-friendly environment, quality of life initiatives, low tax rates and a low cost of living are key drivers to the recent population growth. Walmart, which is headquartered in Bentonville, has weathered the pandemic well which has produced a ripple economic effect throughout the local supplier community. Canoo, an electric vehicle manufacturer, recently announced plans to relocate their headquarters to Bentonville, bringing over 500 new jobs to the area. Housing, especially affordable housing, is one of the biggest economic challenges in this market. In addition, NWA has one of the lowest unemployment rates in the country, and labor constraints are pronounced in the area. The economic outlook for NWA continues to be very promising, primarily limited by the availability of a skilled workforce.

NW Arkansas' year-over-year changes in employment on nonfarm payrolls and employment by major industry sector

Investment Outlook

Our outlook for investment returns in 2022 continues to be optimistic. With a backdrop of continued economic growth and strong consumer balance sheets, we expect market sentiment to continue to remain elevated while earnings grow. The historically low interest rate environment continues to place headwinds on fixed income assets, however, it remains a positive catalyst for supporting equity valuations.

Equities

U.S. equities enjoyed a very good year in 2021 as the major indices rose and volatility returned to more normalized levels. Entering 2022, U.S. equities appear to be at the upper end of fair-value range as they are coming off three consecutive years of above-average returns. Consumer balance sheets have improved dramatically from the onset of the pandemic as consumers have refinanced debt and benefitted from fiscal stimulus. Record levels of cash in households may contribute towards flows into the market or into the economy through spending. As a result, the outlook for valuations and corporate earnings continues to be strong, which should provide support for continued growth in the equity markets.

Given the long period of outperformance of U.S. large cap equities, excessive concentration risk may exist in some portfolios. Developed international equities may be positioned to outperform U.S. stocks due to more attractive valuations. China continues to dominate emerging market dynamics, but active investment management should help mitigate regional risk during continued periods of high volatility.

Fixed Income

The 2021 year proved to be challenging for fixed income investors. Portfolios struggled to provide positive returns as interest rates moved up from very low levels. Interest rates should continue to move higher in 2022 as the Federal Reserve tapers their asset purchases at a rate commensurate with higher near-term inflation expectations and improving economic growth expectations. In response, fixed Income yields will likely increase but remain well below historical averages for the foreseeable future.

Corporations have built up cash reserves, so balance sheets are healthy, resulting in historically low levels of credit defaults. For this reason, credit risk still looks attractive in comparison to interest rate risk. High quality municipal bonds remain a viable investment for high-tax-bracket investors. Investors should view fixed income as a risk-mitigation tool rather than a source of excess returns in 2022. While cash rates are still near zero, there has been meaningful improvement in yield in other short-term instruments, such as money markets and short-term CDs.

Private Capital

Private capital gives accredited investors and qualified purchasers access to a set of investments which provide a portfolio diversification and return premium not found in public markets. The opportunity-set for investors to gain access to private companies has grown significantly over the past decade and is expected to continue to be a significant influence within the entire financial marketplace. A full spectrum of companies, ranging from the smallest to the largest are choosing to stay private longer, or choosing to leave the public markets and going private to provide better returns for shareholders. While the private capital markets do not provide the liquidity associated with public markets, the private capital markets may represent an attractive investment option for a portion of the portfolio for those investors not requiring immediate liquidity.

Portfolio Considerations

With the economic recovery well underway, 2022 should mark the return to a more normalized investment environment. However, investors face many challenges to navigate this year. Equity valuations are high but continued corporate earnings growth should provide support for additional returns in 2022. Exposure to a diversified basket of equities is as relevant as ever with a focus on valuations. Compelling valuations exist outside the U.S., particularly in developed international economies. Additionally, even with anticipated low yields, high-quality fixed income investments still serve as a stabilizer in portfolios. In periods of muted market returns and expected high volatility, thoughtful tax management will play a larger role in overall portfolio returns.

We believe the patient investor should be rewarded in 2022 for sticking with a diversified investment strategy – one which has been designed to match investment goals with personal risk tolerance. While we have attempted to outline the key factors that will be in play in 2022, it is likely that the new year will be defined by other factors that are unknown. In times of uncertainty, surrounding oneself with knowledgeable and dedicated advisors seems prudent.

The INTRUST 2022 Economic Outlook is the consensus of the INTRUST Bank, N.A. (“INTRUST”) Investment Strategy team and is based on third-party sources believed to be reliable. INTRUST has relied upon and assumed, without independent verification, the accuracy and completeness of this third-party information. INTRUST makes no warranties with regard to the information or results obtained by its use and disclaims any and all liability arising out of the use of, or reliance on the information. The information presented has been prepared for informational purposes only. It should not be relied upon as a recommendation to buy or sell securities or to participate in any investment strategy. The forward-looking perspectives are not intended to, and should not, form a primary basis for any investment decisions. This information should not be construed as investment, legal, tax or accounting advice. Past performance is no guarantee of future results.

| Not FDIC Insured | No Bank Guarantee | May Lose Value |

Posted:

12/22/2021

Category:

Recommended Articles